[ad_1]

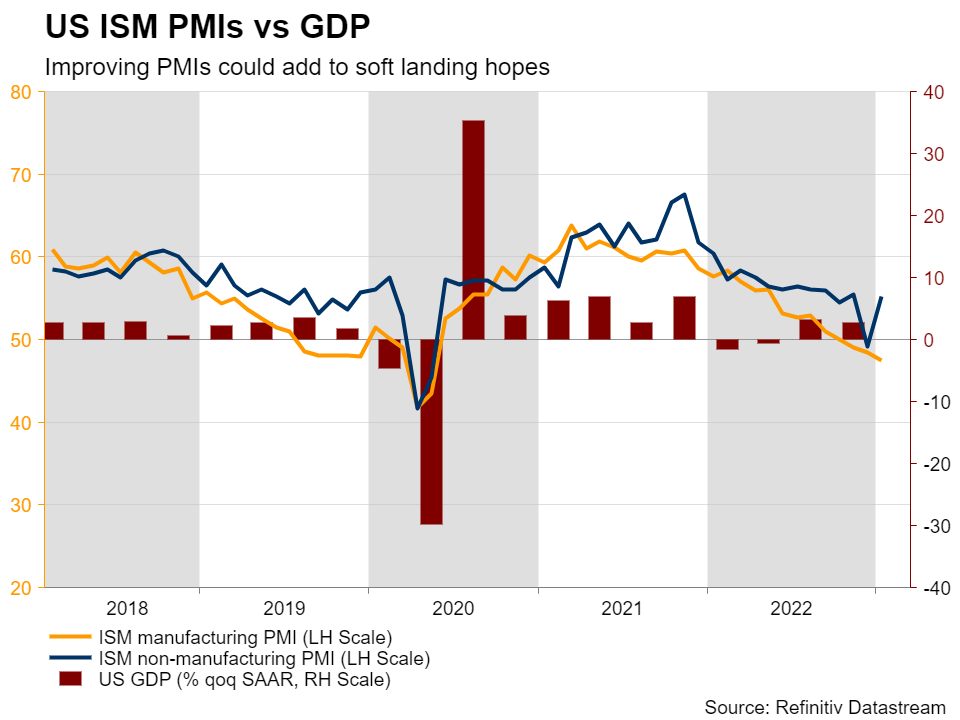

Following a comparatively busy week, the calendar turns into lighter subsequent week. Nevertheless, that doesn’t imply there are not any necessary financial releases on the agenda. Quite the opposite, with market individuals making an attempt to determine what number of extra fee hikes the US economic system can stand up to, they might pay further consideration to the ISM PMIs for February. Additionally, with most ECB policymakers arguing that extra 50bps price of fee hikes are wanted to tame inflation, the Eurozone’s preliminary CPI numbers for February will doubtless take heart stage as nicely.ISM PMIs the greenback’s subsequent testGetting the ball rolling with the US, final week, the preliminary S&P International PMIs shocked to the upside, with the composite index coming back from contractionary to expansionary territory. This was the newest piece of information confirming buyers’ choice to drastically revise up their implied fee path projections. With January CPI information additionally suggesting that inflation is stickier than beforehand anticipated, they’re now anticipating rates of interest to peak at round 5.35% in July, whereas they see them ending the yr at 5.15%.

In that respect, the ISM PMIs on Wednesday and Friday are prone to entice particular consideration. Will they affirm or contradict the S&P International indices? The forecasts level to a combined image, with the manufacturing PMI anticipated to have risen to 47.9 from 47.4, and the non-manufacturing PMI anticipated to have declined to 54.2 from 55.2. Nonetheless, on condition that the companies index accounts for practically 80% of US GDP, one other print decently above 50 is unlikely to change a lot expectations in regards to the Fed’s future plan of action.

The sturdy items orders for January and the Convention Board client confidence index for February are additionally popping out on Monday and Tuesday respectively.

Something including to hopes that the US is prone to dodge a extreme recession may assist the US greenback on hypothesis that the Fed will proceed elevating rates of interest at ranges increased than it projected in December. That stated, arguing a few full-scale bullish reversal within the US greenback stays untimely as forward of the March assembly, the market must digest the employment and CPI experiences for February. On prime of that, the Fed just isn’t the one central financial institution for which buyers have upended their fee hike bets.

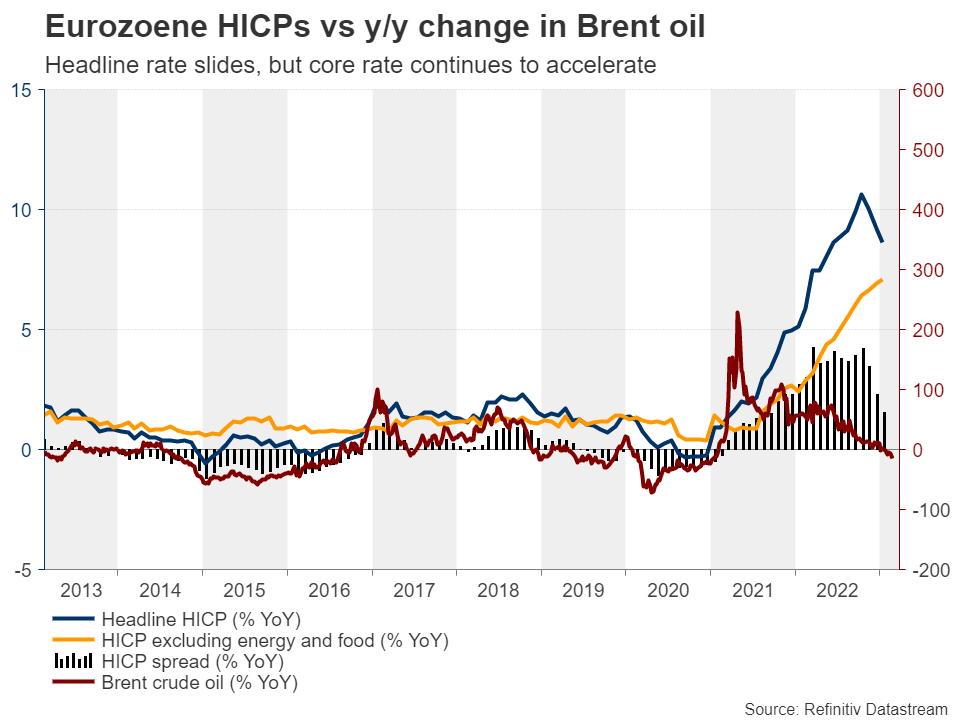

Will Eurozone inflation numbers shake ECB bets?One among them is the ECB. Most ECB officers have been adamant that extra double hikes are wanted, with President Lagarde confirming on the final assembly that one other 50bps hike would be the case in March and several other others hinting at an analogous transfer in Might. The one policymaker sounding a bit cautious was Chief Economist Philip Lane, who famous final week that the Governing Council could not have to proceed as forcefully as earlier than.

Sure, headline inflation has slowed notably after peaking at 10.6% in October and will sluggish even additional within the months to come back because the year-on-year change in oil costs continues to slip. Nonetheless, core inflation is proving tenacious, and Thursday’s information is predicted to disclose a modest slowdown for the month of February to six.9% y/y from 7.1%. The minutes of the newest ECB assembly are additionally on Thursday’s schedule.

Mixed with bettering PMIs within the Euro space, stubbornly excessive underlying inflation and extra hawkish rhetoric by ECB officers may permit buyers to keep up bets a few triple hike on the upcoming assembly. At present, they’re assigning a 30% likelihood for a 75bps increment, with the remaining 70% pointing to 50bps. Additionally they see a complete of 130bps price of extra fee hikes earlier than the Financial institution takes the sidelines, whereas only a week in the past, they have been seeing 100bps.

Rising ECB hike bets are complicating issues for euro/greenback sellers, however in addition they enhance the draw back threat within the case of an upcoming financial launch disappointing. The identical goes for the greenback. Due to this fact, the outlook for euro/greenback appears considerably blurry for now. Possibly each currencies will carry out higher towards the risk-linked ones as growing hike expectations have been weighing on threat sentiment currently. With the slowdown in Canada’s inflation for January congealing expectations that the BoC could chorus from mountain climbing charges additional, the could also be the only option.

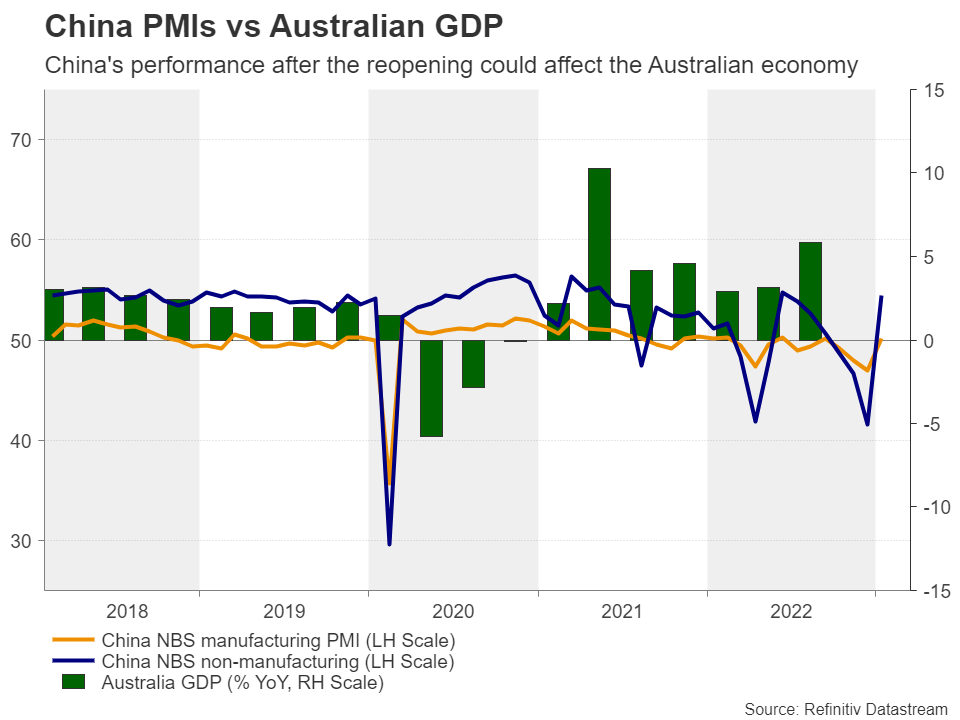

Canadian and Australian GDP, in addition to Chinese language PMIs on tapLoonie merchants may place some hopes on Canada’s GDP figures, however with the m/m fee for December anticipated to have held regular at a modest 0.1% and the annualized q/q fee estimated to have declined to 1.5% from 2.9%, the image for the loonie appears to be like something however vivid.Australia additionally releases GDP information for This autumn, in addition to its CPIs for January. In distinction to the BoC, the RBA raised rates of interest by 25bps and dropped from its assertion a component that put the choice of a pause on the desk, arguing that extra hikes are mandatory within the coming months. So, bettering GDP and additional acceleration in inflation would add credence to that view and maybe permit the to achieve.

That stated, with buyers elevating their bets close to extra aggressive motion by different main central banks as nicely, threat urge for food has been very subdued currently, which is destructive for risk-linked currencies just like the aussie and the loonie. Thus, with the chance commerce turning into a kind of zero-sum sport in aussie/loonie, the Australian foreign money has extra potential to achieve towards its Canadian counterpart slightly than some other risk-linked foreign money, as the principle driving power for this pair would be the divergence in financial coverage between the RBA and the BoC.Aussie merchants may take note of the Chinese language PMIs for February which come out simply an hour after the Australian information. On condition that China is Australia’s principal buying and selling companion, they might be desirous to learn the way the world’s second largest economic system has been performing after the reopening.After Ueda’s testimony, yen merchants flip to the dataFlying from China to Japan, the world’s third largest economic system, subsequent week’s agenda contains the commercial manufacturing and retail gross sales numbers for January on Tuesday and the Tokyo CPIs for February on Friday.At his testimony earlier than the decrease home of the Japanese parliament, BoJ Governor nominee Kazuo Ueda stated that the central financial institution should preserve ultra-low rates of interest to assist the economic system, and whereas it signaled the prospect of tweaking the yield curve management coverage sooner or later, he appeared in no rush to overtake the controversial coverage.So, as buyers attempt to estimate when this might occur, they might pay shut consideration to the aforementioned information, particularly the Tokyo CPI numbers, as they’re an excellent gauge of Nationwide inflation. Though they aren’t a serious market shifting information set, buyers can have a primary glimpse as to the place inflation is headed and whether it is set to proceed to speed up, they might begin speculating a transfer in the direction of normalization sooner slightly than later.

[ad_2]

Source link

{kind=link}