[ad_1]

Olemedia

This previous Wednesday, Blue Orca Capital launched a brief vendor report during which it lobs severe accusations at each Piedmont Lithium Inc (NASDAQ:PLL) and Atlantic Lithium Ltd (OTCQX:ALLIF). The allegations are centered round a Ghanaian property collectively managed by the 2 firms and that’s marginally a part of their bigger Ewoyaa Challenge within the West African nation.

The report, which was categorically denied by each Piedmont and Atlantic, places forth quite a lot of accusations and important evaluation, starting with allegations of impropriety and transferring onto an evaluation its possible penalties. On this article, we’ll overview Blue Orca Capital’s report and talk about what it could imply for Piedmont’s and Atlantic’s inventory costs.

Background

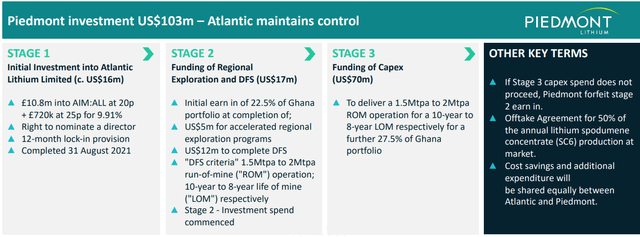

US-based Piedmont is a lithium mining firm with long-term plans to construct a lithium mine and processing facility in Gaston County, North Carolina. Nonetheless, it additionally owns 9.4% of Atlantic Lithium, an Australia-based lithium miner whose major asset is the Ewoyaa Lithium Challenge positioned within the West African nation of Ghana. Piedmont’s curiosity in Atlantic just isn’t a passive funding however slightly half of a bigger deal, outlined within the exhibit under.

Piedmont Investor Presentation

Primarily, what this all boils right down to is that Piedmont may have the flexibility to earn a complete fairness curiosity of fifty% of Atlantic’s Ghanaian spodumene tasks in alternate for funding a big a part of the construct out. This may embrace an offtake settlement for 50% of annual manufacturing at market costs on a life-of-mine foundation. Atlantic has different tenements within the Ivory Coast however Ewoyaa is its major focus. As of December 31, 2022, Piedmont had made funds of $32.9 million to Atlantic as a part of its complete funding dedication.

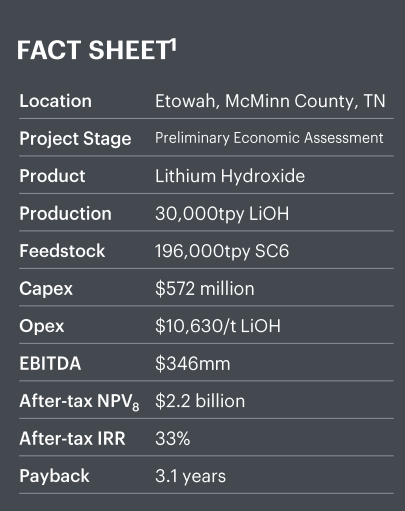

Piedmont intends to ship this offtake to its deliberate Tennessee Lithium plant for conversion to lithium hydroxide. The power, which is within the Preliminary Financial Evaluation part, may have a capability to course of 196ktpa of spodumene focus which can enable it to provide 30ktpa of lithium hydroxide. Building is because of be accomplished in 2025 and manufacturing ought to be absolutely ramped by 2026.

Piedmont’s Tennessee Facility (Piedmont Investor Presentation)

The Foremost Allegation

The first allegation being levelled by Blue Orca is that Atlantic made unlawful funds to the son of a high-ranking Ghanaian politician in alternate for mining licenses. Blue Orca alleges that the person in query, Kwaku Asiedu-Nketiah, acquired these funds by means of the sale of Pleasure Transporters, an organization during which he was an element proprietor and which was bought by Atlantic Lithium.

Blue Orca asserts that:

“In 2021, Atlantic acquired an area Ghana entity, Pleasure Transporters, to acquire mineral rights and licenses on two of the 4 tenements (Saltpond and Cape Coast) for Atlantic’s flagship lithium undertaking in Ghana.

To accumulate Pleasure Transporters, Atlantic paid the homeowners $730,000 in inventory and promised the sellers an extra 2.5% manufacturing royalty doubtlessly value tens of hundreds of thousands of {dollars}.”

Kwaku Asiedu-Nketiah is the son of Johnson Asiedu Nketiah, Chairman of the Nationwide Democratic Congress, and considered one of Ghana’s two major political events. And Blue Orca believes the fee was made as a technique to safe mining permits, as a result of:

“We suspect that Atlantic made these funds to safe the mining permits as a result of, on the time of the transaction, the daddy was not solely a senior get together functionary and former Chairman of the Mines and Vitality Committee of Ghana’s Parliament, however a high-profile determine with specific affect inside Ghana’s mining sector.”

The report goes onto notice that some within the Ghanaian media, in addition to some politicians, have beforehand accused Johnson Asiedu Nketiah of benefitting from corruption. And provided that Asiedu Nketiah’s get together is now not in energy, and that Atlantic has but to hunt ratification for its mining licenses from Ghana’s Parliament, these new allegations of corruption will forestall Atlantic from getting that license. If that have been to happen, it might clearly be a blow from which Atlantic could not recuperate.

The Projected Fallout

The report notes that the fallout would even have a tremendously adverse influence on Piedmont. Along with the possible lack of its Ghanaian investments, Piedmont would haven’t any spodumene for its Tennessee facility.

The report states that, “Ghana offtake is irreplaceable,” and that there’s no approach Piedmont can safe the wanted 196ktpa. Blue Orca spoke with unnamed former Piedmont executives and unnamed consultants and concluded that:

“Provide of spodumene is so tight that if Piedmont loses its Ghana provide, as we suspect it should, Piedmont can’t merely change the Ghana spodumene offtake with a unique producer’s offtake. It’s too late for that – there’s a huge provide scarcity and there’s no longer sufficient close to time period spodumene manufacturing out there for offtake.”

It notes how Piedmont’s share of the lithium to be produced at NAL, one other JV between Piedmont and Sayona Mining Restricted (OTCQB:SYAXF) that is because of ramp manufacturing within the coming months, has already been promised to Tesla Inc. (TSLA). And it seems that Tesla is already constructing a refinery in preparation for receipt of these shipments.

The report goes onto state that the shortcoming to safe offtake for Tennessee, coupled with the shadow solid by Atlantic’s dealings in Ghana, one thing about which Piedmont ought to have been conscious, will imperil its DOE Grant for the Tennessee Facility.

A Essential Evaluation – A Spodumene Scarcity

The report casts each Piedmont and Atlantic in a really poor mild and paints a really bleak image of their respective fates. That is slightly not shocking provided that it is a brief vendor report; in spite of everything, that’s its function. However, if we take a more in-depth take a look at a number of the allegations being made and the evaluation that’s being put forth, we start to rapidly see that issues don’t look fairly so dire.

We’ll start with the straightforward half: the declare that there’s no lithium on the market. And to its credit score, Blue Orca does go right into a good bit of element discussing the foremost lithium tasks as a consequence of come on-line over the subsequent few years. It additionally appropriately notes that a whole lot of their offtake is at present spoken for. Nonetheless, it does rapidly gloss over one main undertaking when it notes that:

“Sigma Lithium has two offtake agreements allocating 230k of its 270k close to time period manufacturing. The corporate plans to considerably increase manufacturing over two future “phases,” however current information reviews counsel that Tesla could quickly have declare to no matter further capability Sigma brings on-line past its present “part 1” manufacturing.”

The extra capability that’s referred to is slightly vital, as might be seen within the exhibit under.

Sigma Manufacturing Profile – 12 months 1 is Subsequent 12 months (Sigma Investor Presentation)

And whereas it is true that current information reviews have mentioned rumors that Tesla could also be focused on shopping for Sigma Lithium, final week, throughout Tesla’s Investor Day, Musk appeared to pour chilly water on that rumor when he famous that the “limiting issue” just isn’t within the inadequate mining of spodumene however slightly restricted lithium refining capability.

Nonetheless, even when Tesla have been to buy Sigma Lithium, there may be the chance that it might select to refine its spodumene at Piedmont’s refinery, if that refinery have been out there. Tesla’s personal refinery can be busy refining spodumene coming from Piedmont’s beforehand talked about NAL mine.

On condition that Brazilian-based Sigma’s operations will hit a run-rate of over 800ktpa in 2027, the issue received’t be discovering spodumene focus, however, slightly, discovering refining capability. In actual fact, the looming addition of Sigma’s and NAL’s lithium to international manufacturing might be a serious contributing issue to the current fall we’ve seen in lithium costs.

A Essential Evaluation – Allegations of Wrongdoing

The second subject that we’ll study are Blue Orca’s allegations of corruption. And that’s precisely what they’re, allegations. I used to be unable to seek out any document indicating that both Johnson Asiedu Nketiah, or his son, Kwaku Asiedu-Nketiah, had been convicted of those crimes or a lot much less even arrested.

Granted, the so-called ‘proof’ supplied in Blue Orca’s report does include a whole lot of allegations by media organisations in addition to Asiedu Nketiah’s political rivals. However that is one thing that may be present in each democracy; even in America, one does not must look far to seek out Democratic media organizations alleging that Donald Trump is corrupt or, by the identical token, Republican media firms making the identical claims about Joe Biden. So, till both Johnson or Kwaku Asiedu Nketiah are convicted by a Ghanaian court docket of regulation, and never by a US-based hedge fund, they are going to be harmless within the eyes of the regulation.

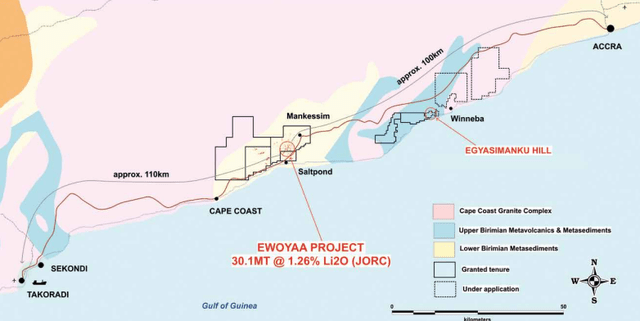

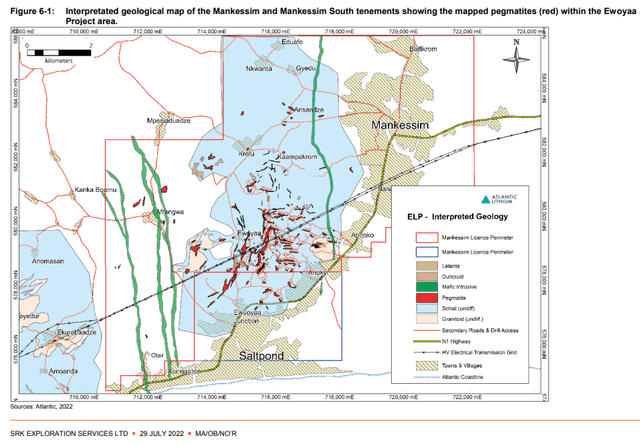

Along with that, the tenements in query, these being the Saltpond and Cape Coast tenements that have been a part of the ‘questionable deal’, will not be even at present part of Atlantic Lithium’s Ewoyaa undertaking and haven’t but been explored.

Atlantic Lithium Tenements (Atlantic Lithium Alternative Prospectus) Ewoyaa Challenge Geological Map (Atlantic Lithium Alternative Prospectus)

Blue Orca’s report calculated a $40 million worth for a royalty granted on the tenements within the deal that it’s questioning, tenements that are unexplored, through the use of the outcomes of Atlantic’s Ewoyaa Pre-Feasibility Examine as a proxy. That is fully ridiculous. Utilizing that logic one can worth the unexplored land instantly beside any mining undertaking on the planet on the identical worth because the mine itself. It assumes that the mineralization beneath the unexplored tenements is strictly the identical as that beneath the explored land on which the mine is to be constructed.

The Drawback

That brings us to the crux of the matter. Blue Orca’s case depends closely on allegations and conjecture. Nonetheless, this will sadly assist it in getting what it desires. All through the report the reader is continually reminded that Atlantic nonetheless requires Ghanaian Parliamentary approval and ratification of its mining license to ensure that the mine to be constructed. Making clear that it is a course of topic to the uncertainties of partisan politics.

By creating the impression that approval of Atlantic’s mine will assist the opposition, Blue Orca’s report could assist change the opinion of some parliamentarians into voting in opposition to approval of the mining license. Additionally, the report itself is an extra doc to which Asiedu Nketiah’s political rivals within the media can level to.

Each Piedmont and Atlantic have rejected the Blue Orca report, however the agency’s marketing campaign can solely serve to complicate the vagaries of parliamentary politics and add higher danger to each of their shares. I had beforehand maintained a Robust Purchase ranking on Piedmont’s inventory and a Purchase ranking on the shares of Atlantic, however this added political danger has pressured me to chop each of their scores to Maintain. Each shares have super potential, however they’ll first must navigate these turbulent waters earlier than they will show that out.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please pay attention to the dangers related to these shares.

[ad_2]

Source link

{kind=link}