[ad_1]

Greenback trades blended towards the opposite majorsPCE numbers and Fed audio system may reshape Fed betsGermany’s CPI information due out a day forward of Eurozone’s inflation numbersWall Road indices add greater than 1% price of beneficial properties every

Greenback awaits the PCE inflation numbers for route

The greenback traded blended towards the opposite main currencies on Wednesday, discovering it laborious to imagine a transparent route as we speak as properly.

The greenback recovered a few of its current losses on Wednesday, as considerations concerning the well being of the US banking sector eased. Nonetheless, traders are nonetheless questioning whether or not the disaster will immediate the Fed to press the pause button quickly and minimize charges later this yr.

Though traders predict rates of interest to finish the yr at the next degree than estimated on the top of the turmoil, they’re nonetheless anticipating round 50bps price of fee reductions by December, whereas they’re evenly cut up on whether or not the Fed ought to ship one other quarter-point hike in Could or take no motion in any respect.

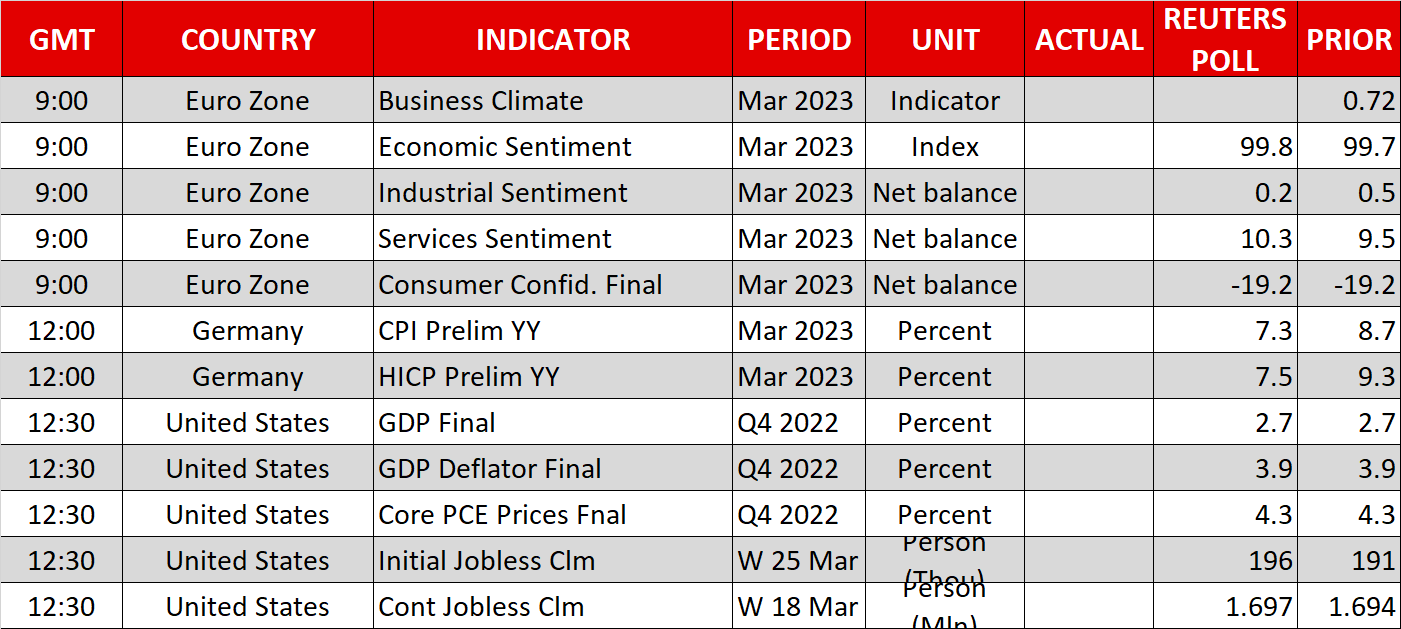

What may represent a further clue to the riddle of how the Fed will proceed henceforth stands out as the PCE inflation information for February, due out tomorrow. The spotlight is more likely to be the core PCE index, which is the Fed’s favourite inflation gauge, with its y/y fee anticipated to have held regular at 4.7%. Nonetheless, with core CPI slowing additional in February, the dangers surrounding the PCE fee could also be tilted to the draw back.

Expectations concerning the Fed’s future plan of action may be affected by policymakers’ remarks. Following Bullard’s feedback that financial coverage will proceed aiming at bringing inflation to heel, Richmond Fed President Thomas Barkin and Minneapolis Fed President Neel Kashkari will step onto the podium as we speak. It will likely be attention-grabbing to see whether or not they’ll sing from Powell’s hymn sheet and push again towards fee cuts bets, but additionally whether or not the market will probably be satisfied.

Eurozone inflation enters the highlight tooEuro merchants are more likely to have a busy finish of the week as properly, as as we speak, the preliminary German CPI information for March are popping out, a day forward of the Eurozone’s numbers.

The forecasts level to a notable slowdown in German inflation, which may elevate hypothesis that the Eurozone’s headline fee will transfer similarly. Nonetheless, with the bloc’s underlying metrics anticipated to have continued accelerating, euro merchants could grow to be extra satisfied concerning the want for extra fee hikes by the ECB, and thereby add to their lengthy positions.

With the yen coming below promoting curiosity because of the easing considerations surrounding the banking trade, euro/yen could climb a bit increased, particularly if the Tokyo CPIs for March, due out early on Friday, gradual additional. Slowing inflation in Japan may enable the BoJ to attend for some time longer earlier than eradicating additional lodging, however with corporations and unions agreeing to the steepest wage enhance in three a long time, taking the case off the desk appears unwise. Subsequently, calling for a long-lasting bullish reversal in yen crosses could also be untimely. In spite of everything, renewed considerations concerning the banking sector can’t be dominated out simply but.

Wall Road jumps as outlook brightensAll three of Wall Road’s most important indices added no less than 1% price of beneficial properties on Wednesday as upbeat outlooks from some companies eased additional considerations concerning the well being of the US economic system.

Micron (NASDAQ:) shares rallied 7.2% after the chip maker projected a drop in Q3 income, however appeared optimistic on the subject of its 2025 outlook, seeing synthetic intelligence to be boosting gross sales, whereas Lululemon Athletica (NASDAQ:) forecast annual gross sales and revenue above Wall Road’s estimates, leading to a 12.7% leap in its shares. Evidently with banking considerations taking the again seat and fee cuts nonetheless on their agenda, traders could really feel extra assured so as to add shares again to their portfolios.

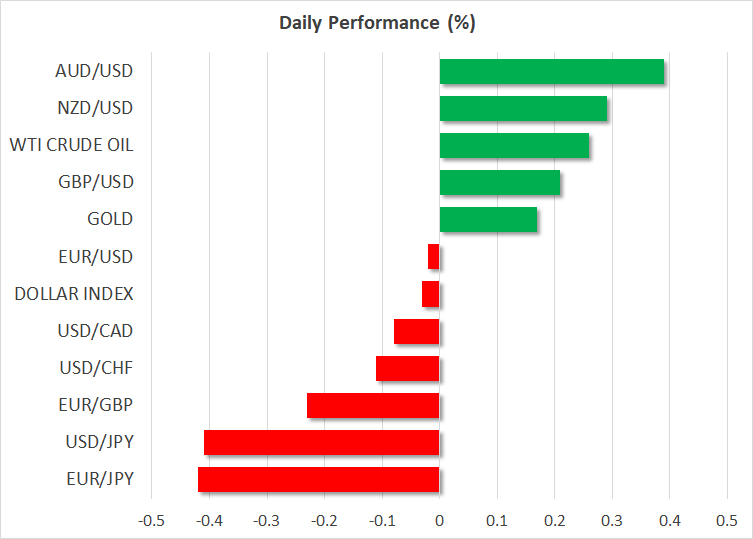

Gold traded considerably decrease yesterday, maybe on safe-haven outflows. Nonetheless, something including credence to the market’s view of a Fed pivot as quickly as this yr may weigh on Treasury yields and the US greenback, thereby maintaining the metallic supported, even in periods when shares are additionally gaining.

[ad_2]

Source link

")

")

{kind=link}