[ad_1]

Subsequent week begins on a quiet observe as Monday is Easter Monday for many economies on our radar. That stated, the calendar turns into heavier as the times move by, with the highlight in all probability falling on the US CPI numbers for March, the minutes from the most recent FOMC gathering, and the BoC resolution. The US information will in all probability represent one other piece of knowledge within the riddle of whether or not the Fed ought to hit the hike button one final time in Could, whereas the BoC resolution could reveal whether or not this would be the main central financial institution to hit the lower button first.Will the US CPIs and Fed minutes corroborate the pivot view?In the beginning of this week, buyers timidly began tilting the size in direction of one other price hike by the Fed at its upcoming gathering in Could, however a streak of disappointing US information thereafter revived doubts on what might be the wisest alternative on the upcoming gathering.

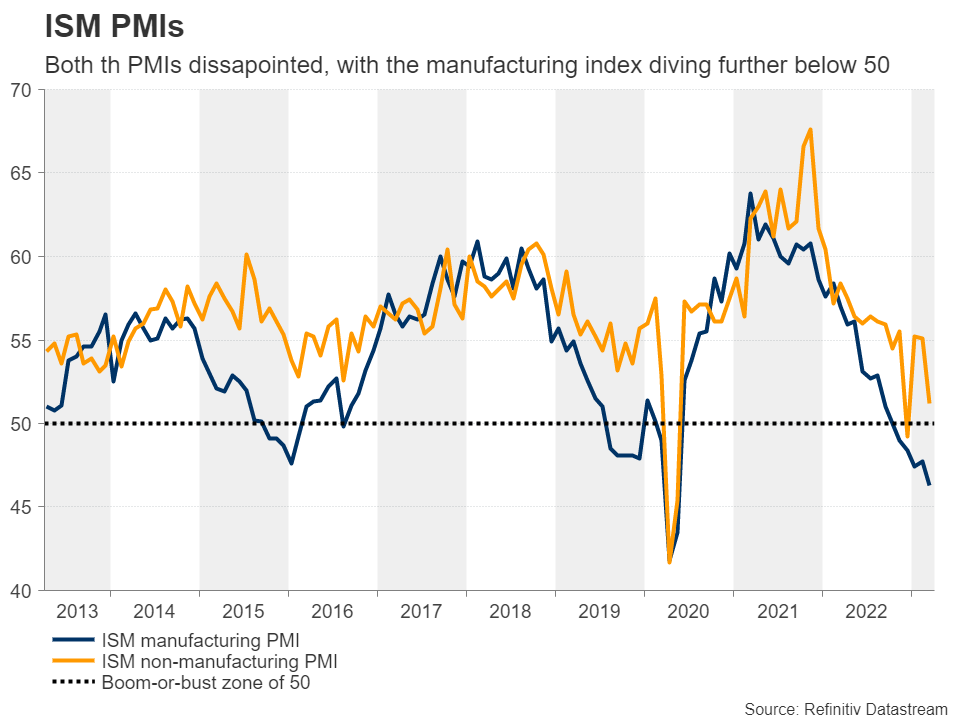

Each the ISM manufacturing and non-manufacturing PMI survey disenchanted on all fronts, from employment to costs, with the outlook of the labor market changing into dimmer after job openings for February slipped to their lowest in almost two years and after the ADP report revealed that the non-public sector gained fewer than anticipated jobs in March and far lower than it did in February.

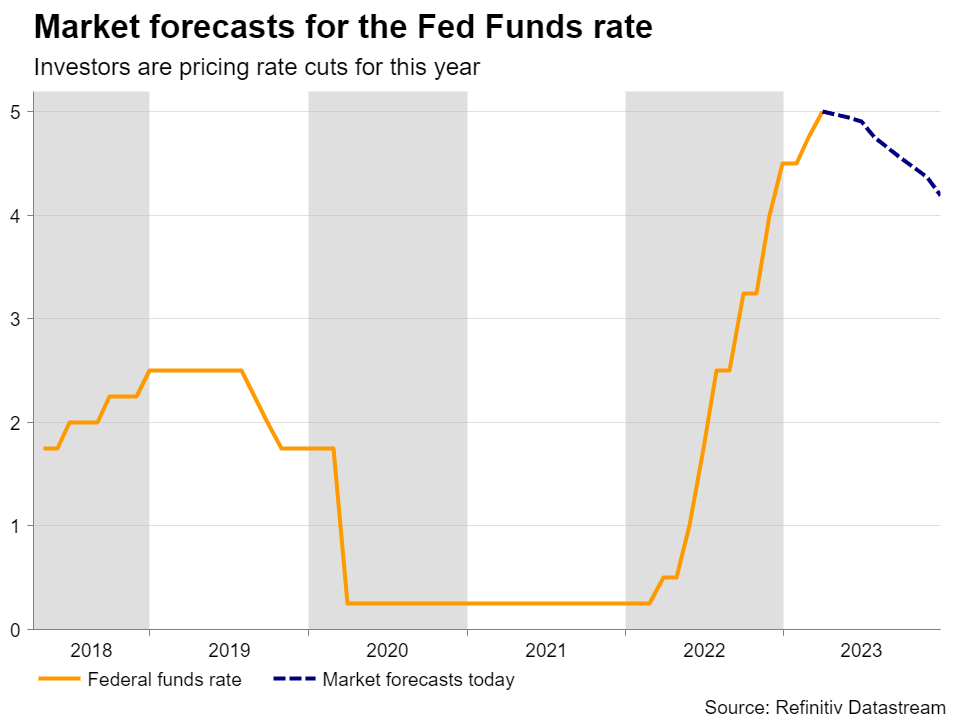

With all that in thoughts, market members are actually evenly break up on whether or not the Fed ought to ship one final 25bps hike in Could or keep sidelined, anticipating a collection of reductions to start out in the summertime, with rates of interest seen ending 2023 at round 4.2%.

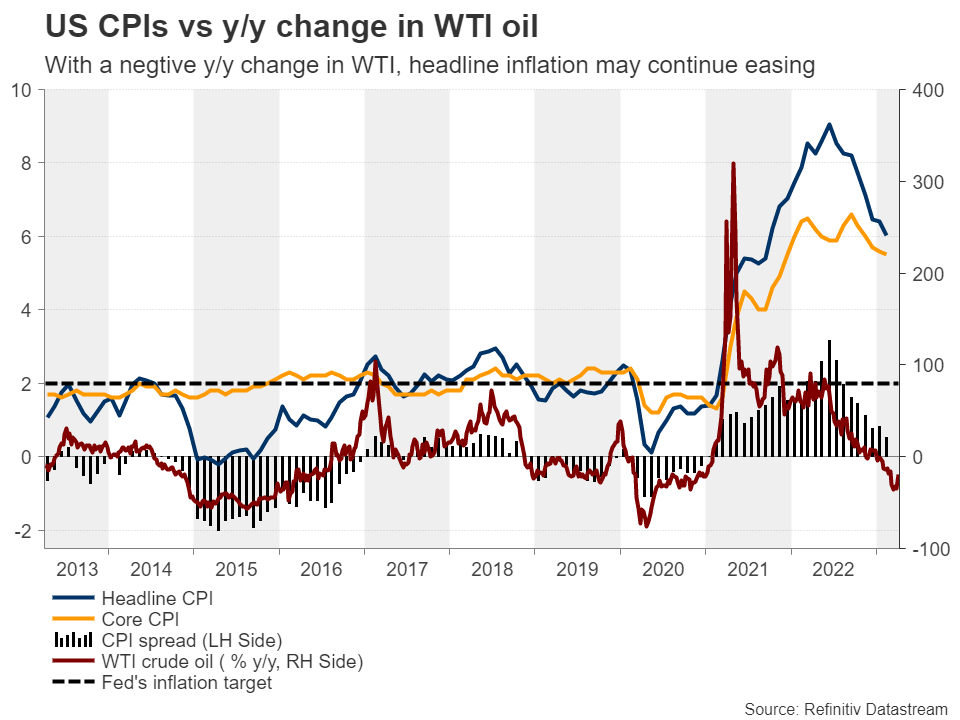

On Wednesday, the CPI information for March are scheduled to be launched, whereas later in the identical day, the Fed will publish the minutes of its newest gathering, the place officers hiked by 25bps, however modified their ahead steerage to notice that future increments ‘could’ be warranted. Coming within the midst of issues concerning the stability of the banking system, the phrase ‘could’ was the important thing to opening the door for a possible pause as quickly as on the subsequent gathering, whilst the brand new “dot plot” and a number of other policymakers within the aftermath of the assembly continued indicating that one other hike is probably going.

Buyers appear to disregard something that pushes in opposition to their view and pay extra consideration to reaffirmations. Thus, they might dig into the minutes to see whether or not officers mentioned the potential for a pause. Additional slowdown in inflation and even the slightest glimpse within the minutes hinting at a the probability of a pause, may add additional credence to the market’s view, thereby sending Treasury yields and the US greenback decrease.

The massive query is how Wall Road merchants will interpret the knowledge. Up till this week, unhealthy information was good for shares on the pondering that decrease rates of interest will end in pricier valuations. Nonetheless, that theme modified this week, with fairness indices coming below stress on fears that the US could also be coming into a deeper-than-previously-feared downturn.

As for the remainder of the US information, Thursday brings the US PPIs for the month, whereas the final check for greenback merchants throughout subsequent week will come within the type of the US retail gross sales and industrial manufacturing for March, in addition to the preliminary UoM client sentiment index for April, all to be launched on Friday.

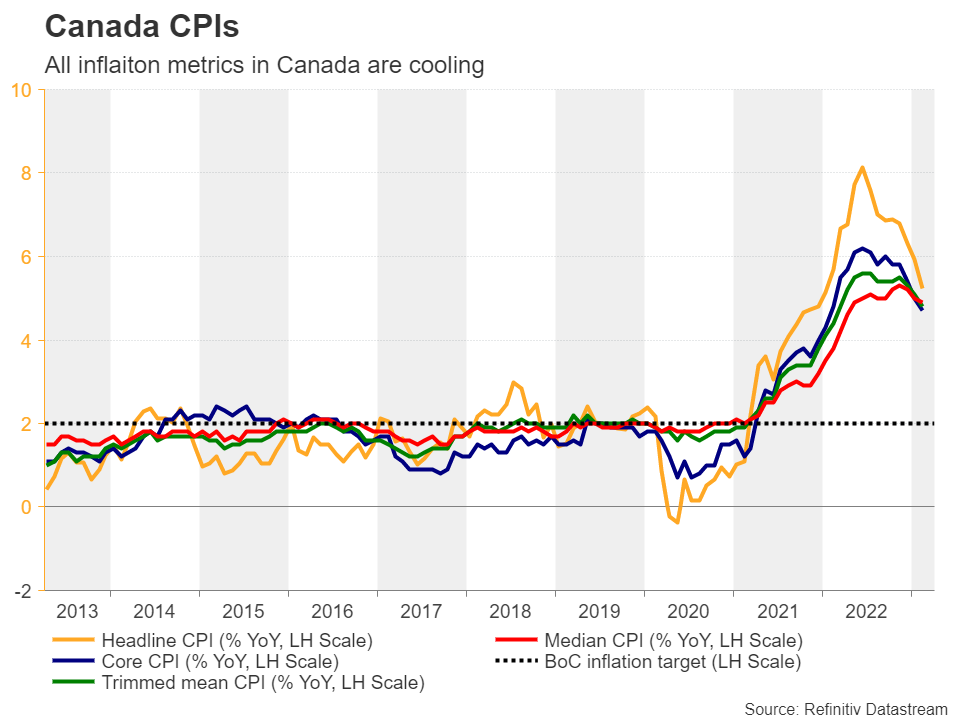

Will the BoC be the primary main central financial institution to start out chopping charges?Wednesday is not going to be a busy day for greenback merchants solely. These having the of their portfolios must keep in entrance of their screens when the BoC decides on rates of interest. At their final assembly, Canadian policymakers determined to maintain rates of interest unchanged, changing into the primary main central financial institution to hit the pause button on this tightening campaign. Though in its assertion, the BoC reiterated it stays ready to extend charges additional if wanted, it additionally stated that the most recent information stays in keeping with the Financial institution’s expectations that CPI inflation will come all the way down to round 3% in the midst of the yr.

Put up-meeting information confirmed that almost all inflation metrics in Canada slowed by greater than anticipated in February, reaffirming the Financial institution’s view and prompting buyers to assign a 15% probability of a price lower as quickly as at subsequent week’s gathering, with the remaining 85% pointing to no motion. Which means if officers determine to maintain rates of interest untouched, any market response could come from hints and clues concerning the Financial institution’s future plan of action. So, something suggesting that they may begin chopping charges quickly may add stress to the Canadian greenback.

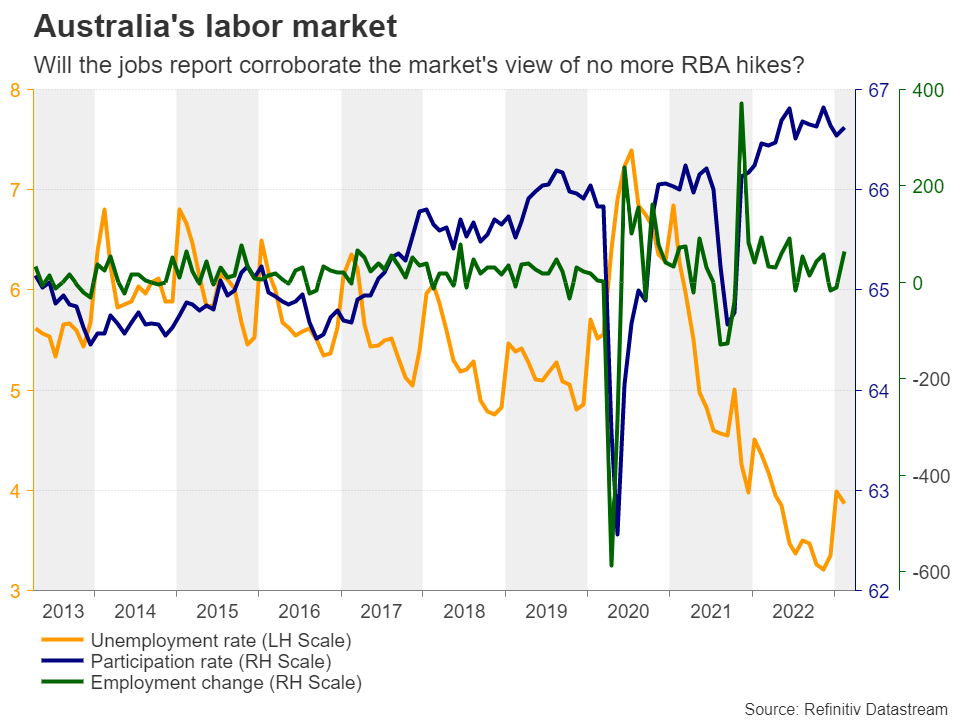

Aussie awaits Australia’s jobs report and China’s inflation numbersWith the RBA standing pat on Tuesday however noting that some additional tightening could also be wanted, merchants could pay additional consideration to the Australian employment report for March scheduled to be launched on Thursday, but in addition on the Chinese language CPI and PPI information, which come on Tuesday, because the world’s second largest economic system is Australia’s foremost buying and selling companion.

The Chinese language CPI is forecast to have accelerated notably, however the PPI is predicted to have remained properly into the unfavorable territory. The previous might be resulting from growing home demand after the economic system’s reopening from the COVID-related restrictions, however placing the latter into the equation, it might be exhausting to determine whether or not Chinese language exports to Australia will gasoline Australian inflation. China’s total commerce steadiness information are popping out on Thursday.

At present buyers are virtually totally satisfied that the RBA is not going to ship every other price will increase. Quite the opposite, they’re almost totally pricing in a quarter-point price discount by the top of this yr, and a weak jobs report may justify that view, thereby hurting the already-wounded aussie much more, particularly in opposition to its New Zealand counterpart, which benefited this week from the RBNZ’s resolution to hike by 50bps and sign that extra hikes are on the playing cards.

Different releases on tapFrom the Eurozone, retail gross sales and industrial manufacturing for February are approaching Tuesday and Thursday, whereas on Thursday, merchants will even get the economic and manufacturing manufacturing figures, the month-to-month GDP, and the commerce steadiness, all for February. With the BoE anticipated to ship greater than 25bps price of extra price increments earlier than it takes the sidelines, pound merchants could search reaffirmation in these releases.

[ad_2]

Source link

{kind=link}