[ad_1]

Printed on November third, 2023 by Bob Ciura

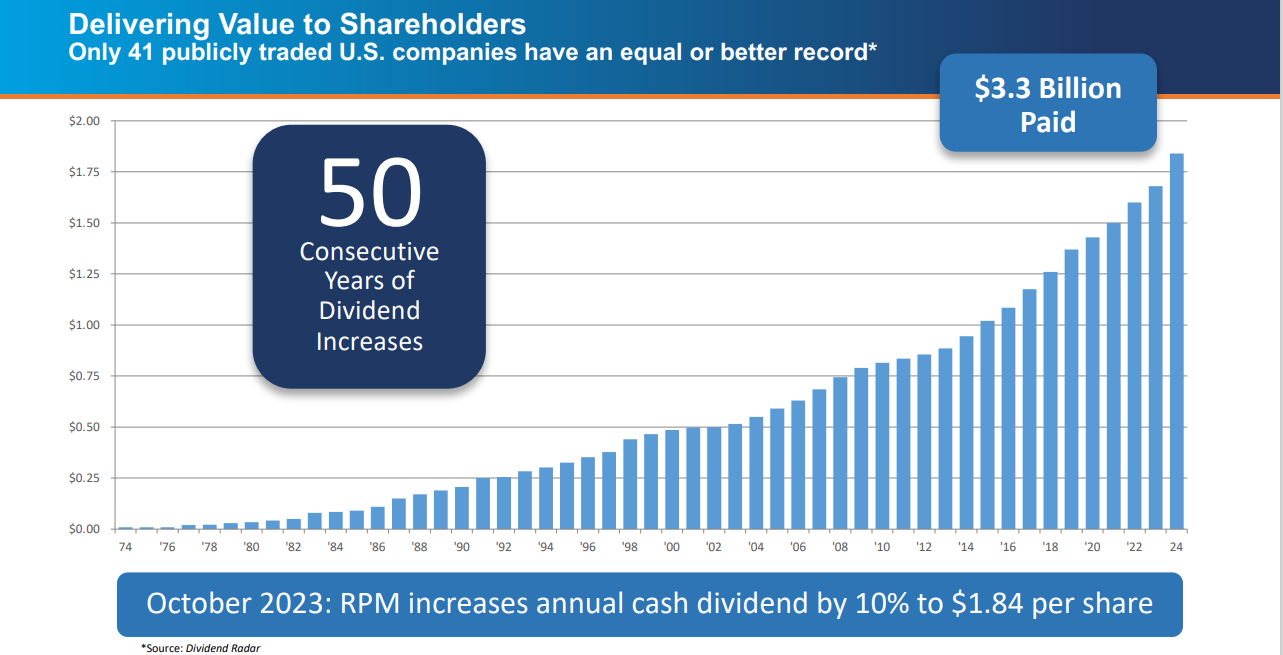

On October fifth, 2023, RPM Worldwide (RPM) introduced that it was growing its quarterly dividend for the fiftieth consecutive years.

Because of this, it has joined the checklist of Dividend Kings.

The Dividend Kings are a gaggle of simply 51 shares which have elevated their dividends for at the very least 50 years in a row. Given this longevity, we consider the Dividend Kings are among the many highest-quality dividend progress shares to purchase and maintain for the long run.

With this in thoughts, we created a full checklist of all 51 Dividend Kings. You may obtain the complete checklist, together with essential monetary metrics similar to dividend yields and price-to-earnings ratios, by clicking on the hyperlink beneath:

RPM is a diversified firm and a frontrunner within the supplies sector. We consider it has a protracted runway of progress up forward, and that it might proceed to be relied upon for annual dividend will increase.

This text will focus on the corporate’s enterprise overview, progress prospects, aggressive benefits, and anticipated returns.

Enterprise Overview

RPM Worldwide manufactures, markets and distributes chemical merchandise to industrial, retail and specialty prospects. The vast majority of gross sales are made to industrial prospects. RPM was based in 1947 and employs greater than 15,000 folks.

Supply: Investor Presentation

On October 4th, 2023, RPM reported earnings outcomes for the primary quarter of fiscal 12 months 2024 for the interval ending August thirty first, 2023. For the quarter, income grew 4.1% to a primary quarter document $2.01 billion, which was $40 million above estimates. Adjusted earnings-per-share of $1.64 in comparison with $1.47 within the prior 12 months, which was $0.10 higher than anticipated.

Three out of 4 segments of the corporate produced document income for the primary quarter. Companywide, natural gross sales improved 3.9% for the interval. Income for the Client Group elevated 1.5% to $670 million. This section had natural progress of 1.7% because of pricing motion.

The Building Merchandise Group grew 10.8% to $783 million. This section had natural progress of 9.5% because of energy in restoration programs for roofing and parking constructions. Efficiency Coatings Group income was up 4.1% to $379 million.

Natural gross sales had been up 4.0% as infrastructure associated companies noticed larger demand. Income of $181 million for Specialty Merchandise Group was a ten.7% lower year-overyear due as soon as once more to decrease volumes in these companies that serve OEM markets. Natural gross sales declined 9%.

RPM now expects gross sales to be up a low single-digit for fiscal 12 months 2024, which is down from a projection of mid-single digit progress. We forecast earnings-per-share of $4.98 for the fiscal 12 months, up from $4.92 beforehand. This might be a 15.8% improve from the prior 12 months.

Development Prospects

Lately, progress has been a lot steadier. From fiscal 12 months 2014 to fiscal 12 months 2023, earnings per share grew at a fee of seven.0% per 12 months. That progress fee has accelerated to 10.1% over simply the final 5 years.

Factoring within the energy of latest outcomes with the seemingly declines in earnings in the course of the subsequent recession, we now forecast annual earnings progress of seven%, up from 5%, by fiscal 12 months 2029.

Natural income progress is predicted to be the first contributor. Increasing revenue margins may even play a key position within the firm’s future EPS progress.

Supply: Investor Presentation

Development slowed over the past recession, however RPM was capable of preserve and improve its dividend funds to shareholders even in an antagonistic financial local weather.

Aggressive Benefits & Recession Efficiency

RPM is a number one producer and distributor of paints, coatings, development chemical compounds, colorants and adhesives to shoppers, contractors, and development companies. These companies carry out effectively when the economic system is rising as a result of will increase in development and residential enchancment spending.

Nonetheless, RPM could be very vulnerable to recessions. You may see the corporate’s earnings-per-share efficiency in the course of the Nice Recession beneath:

2007 earnings-per-share of $1.64

2008 earnings-per-share of $0.36 (78% decline)

2009 earnings-per-share of $0.93 (158% improve)

2010 earnings-per-share of $1.39 (49% improve)

As you’ll be able to see, the corporate’s earnings-per-share declined considerably in 2008, however recovered within the following two years because the economic system emerged from the recession.

We count on this recession-resistant Dividend King to carry out equally throughout future downturns within the enterprise setting.

RPM will not be recession proof, as proven by the corporate’s decline in earnings, and within the time that it took for earnings progress to return to the corporate following the final recession. The corporate additionally has a excessive degree of debt that would make acquisitions or excessive dividend progress tough if earnings had been to weaken.

From a dividend perspective, RPM’s dividend additionally seems very protected.

Supply: Investor Presentation

The corporate has a projected dividend payout ratio of 37% for 2023. RPM has raised its dividend for 50 consecutive years.

Valuation & Anticipated Complete Returns

Primarily based on anticipated EPS of $4.98 for 2023, RPM inventory trades for a price-to-earnings ratio of 19.4. We reaffirm our goal P/E of 20 as that is extra in-line with the long-term common valuation and displays the standard of earnings outcomes over the previous few years.

If the inventory had been commerce with this a number of by fiscal 2029, then valuation can be a 0.6% tailwind to annual returns over this era.

The opposite main part of RPM’s future whole returns would be the firm’s earnings-per-share progress. We count on 7% annual EPS progress for the corporate.

Lastly, whole returns will obtain a lift from the corporate’s dividend funds. RPM shares presently yield 2%.

General, RPM’s anticipated whole returns might be composed of:

7.0% earnings-per-share progress

2.0% dividend yield

0.6% a number of reversion

Complete anticipated annual returns are forecasted at 9.6% per 12 months over the subsequent 5 years. We now fee RPM a maintain.

Closing Ideas

RPM Worldwide continues to ship document setting outcomes, a powerful feat contemplating the expansion charges that the corporate skilled final fiscal 12 months. The corporate has a powerful dividend progress streak as effectively.

With anticipated returns just under our 10% purchase threshold, we presently fee RPM inventory a maintain.

If you’re fascinated about discovering extra high-quality dividend progress shares appropriate for long-term funding, the next Positive Dividend databases will likely be helpful:

The key home inventory market indices are one other stable useful resource for locating funding concepts. Positive Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

[ad_2]

Source link

{kind=link}