[ad_1]

Justin Sullivan

Whereas CEO Elon Musk stay a little bit of a controversial determine, Tesla, Inc. (NASDAQ:TSLA) seems effectively set as much as dominate the high-end electrical car (“EV”) market, whereas different progress areas are rising. One space of explicit benefit is its Supercharger community.

Firm Profile

Tesla designs and manufactures battery electrical autos (BEVs). It presently provides 5 fashions: Mannequin 3, Y, S X, and Cybertruck.

It additionally provides lithium-ion battery power storage via its Powerwall and Megapack merchandise. Powerwall is designed for residence use, whereas Megapack is a industrial grade answer. The corporate additionally sells photo voltaic methods.

Alternatives

Relating to alternatives, TSLA has many. As a frontrunner in digital autos that has been on the forefront of advancing the know-how, it ought to profit as international locations across the globe have set targets to extend EV manufacturing. Quite a few nations have set targets to part out the sale of combustible-engine autos, with the European Union having a mandate that every one new autos gross sales be EVs by 2035. Solely about 6% of vehicles gross sales within the U.S. are EVs, whereas the Europe Union is simply about 12%. China, in the meantime, has develop into the biggest EV market on this planet. Whereas different automobile firms will inevitably take some share, TSLA continues to be set to be one of many main beneficiaries of the worldwide push in direction of EVs.

The corporate additionally seems like it’s on the precipice of reworking the automobile manufacturing course of via its use of gigacasting, which replaces welded parts via aluminum die casting. The intention is to scale back the associated fee the price of a car chassis by as a lot as 40%. TSLA can already manufacture its Mannequin Y in solely 10 hours, which is thrice faster than its rivals. This new method would simply give it a good greater price benefit over its rivals.

Autonomous driving and its FSD (full self-driving) platform is one other potential progress driver. Model 12 of FSD is presently being examined by staff and is anticipated to be rolled out to the general public quickly. The corporate is decreasing the worth to get folks to attempt the platform, though it indicated that the worth will go up proportionate with its worth. It is a cutting-edge characteristic this can be a very long time within the making that ought to draw a whole lot of curiosity from present TSLA drivers. It is also a characteristic that ought to drive demand for its autos as effectively. TSLA has mentioned that it’s keen to license this know-how to different OEMs as effectively.

Different areas of potential alternative embody its new supercomputer Tesla Dojo, in addition to Megapack. Telsa Dojo is the supercomputer behind the machine studying and AI fashions for its self-driving system. It is going to be attention-grabbing to see if it takes this know-how to different areas. Megapack, in the meantime, is a battery and storage system that may assist stop grid outages. Grid integrity is a large international subject, and Megapack might play an enormous half within the answer. TSLA power storage enterprise has been robust, with report deployments of 4GWh in Q3, and it introduced an enormous order win in December.

Maybe the chance I am most enthusiastic about, although, is TSLA’s supercharging community. It has the biggest charging community by far. In truth, its U.S. charging community is bigger than all others mixed. The corporate’s community now stands at 5,000 places and 50,000 connectors. This has develop into a properly worthwhile enterprise, and it ought to develop into an enormous grower within the years forward. The corporate well opened up its community to different OEMs, which is able to solely drive extra utilization. It might additionally assist hasten much more EV adoption.

Proudly owning the biggest charging infrastructure community is a large benefit for TSLA in my opinion. As international locations push to 100% EV gross sales within the coming a long time, these charging networks are prone to play an even bigger and greater function. The reason being easy, if you happen to reside in a significant metropolis or an residence, in-home charging very effectively will not be an choice. As charging tech will get higher and sooner within the years to return, these EV house owners are going to have to make use of charging stations to energy their vehicles.

It is usually possible that whereas TSLA has opened up its charging community that its autos will most probably work finest with the infrastructure it has constructed. On the similar time, opening up its charging community possible means that it’ll considerably decelerate the tempo of different firms ramping up their charging networks now that they now not must spend the cash. Years down the highway, although, this could drastically profit TSLA gross sales to the big proportion of the inhabitants the place in-come charging will not be an choice.

This could finally result in a pleasant recurring income stream for the corporate. It might be very akin to Ford (F) or GM (GM) within the early days of the auto taking management of the gasoline station and fueling infrastructure.

Dangers

Relating to dangers, CEO Elon Musk is entrance and middle. The early investor who wrest management of the corporate has an virtually cult-like following. Relating to key-man danger, there will not be firm with a bigger one right now.

Musk has confirmed to be a visionary, and he has turned TSLA into one of the crucial helpful firms on this planet. On the similar time, Musk is a controversial determine. No matter whether or not you like him or hate him, Musk is the driving pressure at TSLA, and if something occurs that takes him away from his function as CEO, the inventory would possible take successful.

One other danger is the financial system. TSLA nonetheless sells autos, so if the financial system worsens, automobile gross sales can actually go down as effectively. And as with all car producer, there can be manufacturing and provide chain disruptions.

The EV market additionally has a little bit of a used automobile drawback, in that many patrons are a bit cautious shopping for used EVs. The battery makes up about 30% of the price of an EV, and lots of patrons are reticent about used EVs given older battery tech and battery degradation over time. Used Teslas typically promote higher than different used EVs, however the used EV market and its impression on the brand new EV market is one thing to observe within the years forward.

And regardless of the worldwide authorities push in direction of EV adoption, there are points that stand in its manner. One, as famous above, is that not everybody has entry to residence charging, with J.D. Energy saying that just one in three automobile house owners has the power to cost a automobile at residence. Given the time it presently takes to cost a car, this develop into an enormous inconvenience if somebody must solely use supercharger stations. In the meantime, even with authorities subsidies, costs for EVs are sometimes dearer than their flamable engine counterparts in lots of areas – though in some states they are often fairly the cut price.

Being in an trade that’s nonetheless reliant on subsidies is a danger as effectively. I don’t see subsidies going away given the federal government push to get extra EVs gross sales, however it’s not out of the realm of risk and state subsidies additionally play an enormous function in EV gross sales as effectively.

Competitors is a danger as effectively. Each conventional automakers and start-ups are placing extra assets into EVs. Nonetheless, TSLA has each the tech and model lead within the house, which might be tough to beat. Nonetheless, in China, it might be a unique story, with home participant BYD Firm Restricted (BYDDF, BYDDY) turning into the world’s largest producer of EVs in This fall.

Valuation

TSLA presently trades at an EV/EBITDA a number of of 33x the 2024 consensus of $20.56 billion. Primarily based on 2025 EBITDA projections of $29.54 billion, it trades at a 23x a number of.

On a P/E foundation, the corporate trades at 56.4x the 2024 consensus of $3.88 and 41.2x the 2025 consensus of $5.31.

Income is projected to develop over 20.8% in 2024 and 22.9% in 2025. Tesla studies its This fall 2023 outcomes post-market on January twenty fourth.

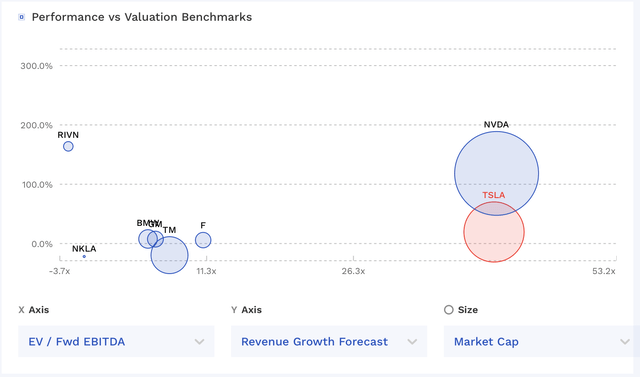

If you wish to evaluate TSLA to different automakers, it trades at an enormous premium. Nonetheless, TSLA is greater than a carmaker, it’s a visionary firm on the forefront of some main developments. And in that regard, it might be finest to match it to an organization like Nvidia (NVDA), which is the dominant participant in GPU chips getting used to energy AI purposes. In that regard, the 2 firms commerce at related multiples, though NVDA is anticipated to develop extra rapidly subsequent 12 months earlier than they each settle into that 20% vary. You’ll be able to learn extra on my ideas on NVDA right here.

TSLA Valuation Vs Friends (FinBox)

Given its progress and benefits, and understanding that TSLA is far more than a automobile firm however a visionary firm, I’d worth the inventory between 25-30x 2024 EBITDA. That would place a good worth vary on the inventory between $238-285.

Conclusion

After a tough 2022 for the inventory, TSLA rebounded properly in 2023. With 2024 upon us, I believe it’s honest to say the inventory had gotten forward of itself at instances after the pandemic. Nonetheless, the corporate and Musk have been capable of show the doubters flawed, and TSLA has proven that it has constantly been capable of develop into its valuation.

TSLA has a whole lot of innovation that appears prefer it ought to assist energy the corporate going ahead, from self-driving, to its supercharger community, to supercomputers, to grid stage battery storage. I am notably enthusiastic about its Supercharger community, however there are a selection of causes to be upbeat concerning the firm. In truth, it might be one of the crucial thrilling instances to be a TSLA investor.

At the moment, I’m going to begin TSLA with a “Purchase” score and $285 worth goal, as I believe the positives outweigh the dangers.

[ad_2]

Source link

{kind=link}