[ad_1]

Justin Sullivan

Adobe (NASDAQ:ADBE) shares dropped by greater than 13% once they introduced their Q1 FY24 earnings on March fifteenth. I mentioned my bullish view on Adobe in my article revealed in December 2023, indicating their progress from AI and pricing improve. Regardless of their Q2 outlook being decrease than the market anticipated, I’m fairly optimistic about their AI progress potential. Contemplating the worth drop, I’m upgrading Adobe inventory to ‘Robust Purchase’ with a good worth of $600 per share.

Robust Q1 Development and Dissatisfied Internet ARR Steering for Q2

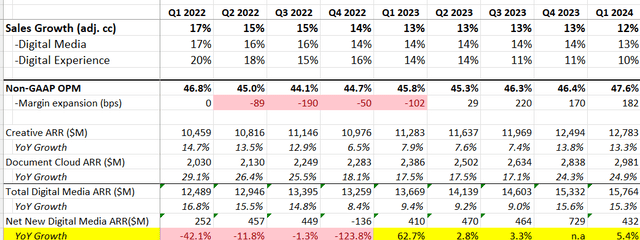

In Q1 FY24, they delivered 12% income progress on a continuing forex foundation, and their margin expanded by 182bps YoY, as summarized within the desk under. Annualized Recurring Income (ARR) is the important thing main indicator for Adobe, and their artistic ARR was up 13.3% YoY and doc cloud ARR elevated by 24.9%. A fairly sturdy lead to Q1 certainly!

Adobe Quarterly Earnings

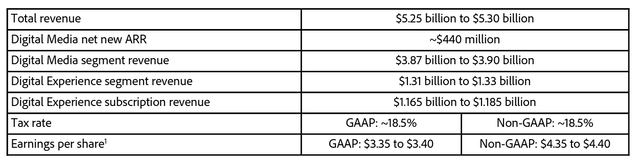

As illustrated within the Q2 steering desk under, Adobe guides round 9% income progress, and $440 million digital medial internet new ARR for Q2 FY24. The market is sort of disenchanted with the online new ARR steering, which signifies 6.4% decline year-over-year.

Adobe Q1 FY24 Incomes Launch

The important thing cause for such weak ARR progress is because of the normalization of their pricing progress.

Adobe began to lift their product worth from FY22, and a few pricing actions have been rolled out in FY23. These pricing will increase have contributed extra progress to their topline over the previous two years. As mentioned in my earlier article, Adobe raised their Inventive Cloud subscription worth in FY23. With out additional pricing changes, Adobe is predicted to normalize their pricing progress in FY24, which might create some progress headwinds resulting from excessive comparables. Their weak ARR steering is extra prone to be a math difficulty, not attributable to any elementary points.

AI Monetization Is on the Early Stage

As talked about in my earlier article, Adobe has been closely investing in AI associated tasks. Adobe has built-in their Firefly into each Inventive Cloud and Adobe Categorical, and Firefly has been used to generate 6.5 billion items of media as disclosed over the earnings name. Moreover, Adobe expressed that they skilled the very best adoption price of Firefly powered by Photoshop in Q1 since its launch in Might 2023. It’s fairly spectacular to see the sturdy adoption of Firefly, an influence software to make the most of AI to generate photographs. Adobe plans to develop Firefly into all of their fundamental merchandise over time, and the sturdy adoption price paves the best way for his or her future monetization.

Adobe additionally launched AI Assistant in Acrobat, geared toward helping customers to simplify duties equivalent to search and share paperwork. The administration is sort of assured that Adobe has super alternatives for monetization amongst their core base of Acrobat customers.

All these AI-related tasks are nonetheless within the early stage, and presently, I don’t anticipate these options/merchandise producing notable progress for the corporate. Nevertheless, I acknowledge these AI-powered options would make it simpler for customers to create digital contents. Adobe ought to have the ability to monetize these subscription-based merchandise sooner or later as it may possibly add worth for individuals who need to create digital contents.

Is Sora a Large Risk?

Sora, OpenAI’s text-to-video mannequin, has attracted a lot of attentions lately. The development of AI expertise makes it attainable to create digital contents a lot simpler than earlier than. There are some considerations that Sora might probably disrupt Adobe’s Inventive Cloud enterprise. Is that an actual risk?

Sora remains to be within the personal beta, and it will be too early to evaluate its performance. However basically, customers can generate a video based mostly on the inputs equivalent to surroundings, actions or topics.

Sora is just not the primary to use AI to video contents. Runway was based in 2018, and the corporate focuses on AI fashions for producing video and pictures. Their video modifying instruments have been utilized in some films, equivalent to “The whole lot All over the place All at As soon as”. Runway has additionally launched AI instruments for public customers, providing image-to-video and text-to-video fashions.

I believe the general risk to Adobe’s Inventive Cloud enterprise is sort of restricted.

Adobe has been closely investing in AI expertise, leveraging notable aggressive benefits equivalent to information and large digital content material repositories. These property might be probably utilized for AI machine learnings. Through the earnings name, Adobe’s administration indicated that the corporate is collaborating with OpenAI relating to Sora, and each Adobe and OpenAI are creating their very own fashions.

Even sooner or later when customers can create contents from texts or some easy inputs, they’d nonetheless require Adobe’s Inventive instruments to edit these movies. The AI-powered video instruments ought to be seen as complementary to Adobe’s Inventive Cloud options, for my part.

$25B Shares Repurchase and Outlook

Adobe introduced a brand new $25 billion shares repurchase plan, representing round 11% of whole market cap. Assuming they full the shares repurchase over the following 4 years, the overall rely of shares excellent might be decreased by 3% yearly, as per my calculation. A fairly spectacular capital allocation!

One other takeaway from Q1 FY24 is their sturdy FCF progress. Excluding the $1 billion break-up price with Figma, their working money move was up 28% year-over-year. Their administration indicated that the sturdy deferred income and unbilled backlog contributed to their sturdy money move progress for the quarter.

For the FY24, I forecast they’ll ship 10% natural income progress, which represents a deceleration from 13% progress achieved in FY23. The deceleration displays their pricing improve advantages in FY23, and the comparables headwinds in FY24. Adobe goes to ramp up their Categorical Cellular and AI Assistant within the second half of FY24, anticipating these AI-related options to contribute to their ARR progress from the second half of the yr. I don’t assume any materials modifications in macro atmosphere or enterprise digital advertising spending in FY24. As such, if excluding 3% pricing progress in FY23, Adobe ought to have the ability to ship 10% natural income progress even with none contribution from AI options.

Valuation Replace

As mentioned beforehand, I forecast Adobe to attain 10% natural income progress in FY24. Assuming Adobe allocating 5% of group income in direction of acquisitions, tuck-in offers might attribute 1.3% to the topline progress.

As Adobe plans to repurchase $25 billion of personal shares over the following few years, the shares excellent might be decreased by 3% yearly based on my calculation.

I estimate their working bills will develop by 10.7% year-over-year, leading to 30bps margin enlargement.

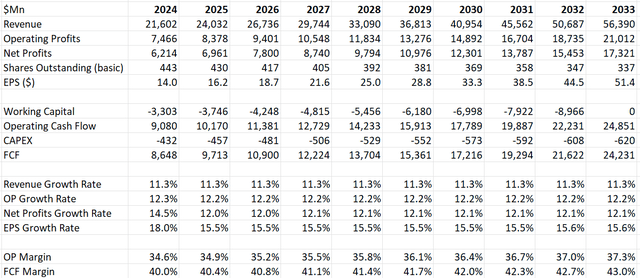

After discounting all of the free money move, the overall fairness worth of Adobe is calculated to be $266 billion, as per my estimate. Thus, the honest worth is estimated to be $600 per share in my mannequin. The present inventory worth is simply buying and selling at 22 occasions FY25’s FCF, a fairly low cost a number of for a double-digit progress firm in my view. It seems to me that the present inventory worth has factored in lots of considerations relating to AI disruptions sooner or later.

Adobe DCF – Writer’s Calculation

Different Points

Figma Break-up Price: Adobe paid $1 billion for the break-up price after they deserted the acquisition plan. I all the time suppose it was not a good suggestion for Adobe to pay a hefty worth to accumulate Figma, and fortunate (or unfortunate for Adobe) the regulator didn’t approve this deal.

Inventory Choices: Adobe spent 8.9% of whole income on SBC in FY23, a rise from 8.2% in FY22. My margin assumption within the DCF mannequin does require their SBC as a proportion of income to say no to six% by FY33. If Adobe continues their excessive SBC payout sooner or later, the honest worth in my DCF mannequin can be overestimated.

Conclusion

Adobe’s AI expertise remains to be within the early stage, they usually have the potential to monetize their present AI investments within the close to future, in my view. I proceed to view Adobe as a high-quality progress firm, and I improve Adobe to ‘Robust Purchase’ with a good worth of $600 per share.

[ad_2]

Source link

{kind=link}