[ad_1]

BeritK/iStock through Getty Photos

Introduction

I’ve been trying ahead to sharing my up to date ideas on Hims & Hers Well being (NYSE:HIMS). I took every week to digest the earnings name with a purpose to make sure that I put collectively a considerate piece. I’ve printed eleven articles on Hims going again to November 2021. To place this in perspective, I’ve solely printed 50 different inventory articles within the six years that I’ve been a author on Looking for Alpha.

To be a profitable investor is to be a disciplined investor. For each one inventory I spend money on, there are tons of I discard. I don’t spend money on or write on shares I haven’t psychotically analyzed from each angle nor do I write articles for the cash. I write as a result of it’s a ardour. Looking for Alpha may pay me free.99 for this text and I’d nonetheless write it (Richard: don’t get any concepts). And talking of cash, I disclosed my unique Hims buy of about 50,000 shares at a value foundation of $5.50.

You are able to do the maths.

Disclosure

In late 2023, I opened my very own registered funding advisory agency, DocShah Monetary. I received’t bore you with the small print, however we’ve had unbelievable progress and formally crossed $1,000,000 in property below administration on March 4, 2024. Integrity is on the core of all the pieces I do, and as such, please be sure to learn my disclosure on the backside.

Benefit from the piece.

“Who The Heck is Hims?”

This was truly a good friend’s response after I stated, “I personal Hims.”

Thankfully for us all, Hims is a ‘what,’ not a ‘who.’

Hims and Hers Well being is a telehealth firm that primarily targets Millennials and Gen Z, providing them well being options in 5 broad classes:

Sexual Wellness (ooh la la) Hair Regrowth Dermatology Psychological Well being Weight Loss

As soon as once more, I may bore you with the small print of how huge the TAM is for every class, however I already did that right here. This text goes to be completely different.

The second you perceive {that a} inventory’s success is twice the byproduct of human psychology as it’s fundamentals, the higher investor you’ll be going ahead.

Millennials and Gen Z are completely different from different generations; for higher or for worse (if we’re worse, I apologize). Most of us grew up remoted. Discover, I didn’t use the phrase, ‘alone.’ We weren’t alone – we had been linked to folks 24/7/365… simply, you already know… by way of a tool.

We had been remoted.

We didn’t want to satisfy in particular person as a result of we may meet by way of a display screen.

What’s the results of this?

As a colleague of mine emailed me:

The result’s, you get a bunch of anxious/nervous individuals who nonetheless want healthcare, however, if given the selection, would 100% select to do it by way of a display screen than in particular person.

And that is precisely what the market didn’t perceive about Hims;

That Hims was an organization born out of necessity. Not of alternative.

And this exactly what I understood at $5 per share;

At $4 per share;

And, as I stood remoted, at $3 per share.

Valuation

We’ll worth Hims through FCF and EPS.

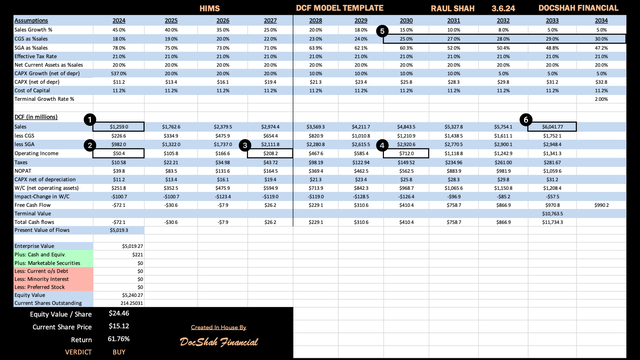

DocShah Monetary’s DCF

DSF HIMS DCF (DocShah Monetary )

I’ve six key checkpoints marked on my DCF with a purpose to hold us in line as we make our approach by way of the subsequent ten years collectively. These six key areas are a mix of steering from each CFO Yemi Okupe and CEO Andrew Dudum through the newest earnings name and my very own forecasts.

Checkpoint 1: 2024 Gross sales

Yemi Okupe’s Steerage:

For the full-year, we’re anticipating income of between $1.17 billion to $1.2 billion.

In my opinion, Yemi’s steering seems overly conservative. To succeed in $1.2 billion in gross sales for 2024, a CAGR of simply 8.3% per quarter can be required. To place this in perspective, Hims averaged quarterly progress charges of 10% final 12 months:

Q1: 14.1% Q2: 9.0% Q3: 9.0% This autumn: 8.8%

The primary quarter tends to have stronger tailwinds and as such, I’d anticipate Hims to put up strong earnings progress. I feel 12.0% is a wise estimate and if we get something close to that quantity, then we may coast the remaining quarters with 6% CAGR progress and nonetheless attain gross sales of $1.2 billion.

My forecast is:

Q1: $276 million (12% sequential improve) Q2: $301 million (9% sequential improve) Q3: $328 million (9% sequential improve) This autumn: $354 million (8% sequential improve)

Complete 2024 gross sales: $1.26 billion

Checkpoint 2: 2024 EBITDA

Yemi Okupe’s Steerage:

It’s our expectation that 2024 adjusted EBITDA shall be between $100 million and $120 million.

I calculated EBIT (working revenue) of $50 million for this 12 months, which roughly equates to $110 million in adjusted EBITDA.

If you’re confused, take the second to learn this, in any other case hold it transferring:

EBITDA excludes depreciation and amortization. Adjusted EBITDA excludes each of these I simply talked about AND contains stock-based compensation. So, with a purpose to reconcile an adjusted EBITDA forecast with an EBIT forecast (working revenue), it’s a must to reverse all these transactions above. Meaning to go from adjusted EBITDA to EBIT, you add again depreciation/amortization and subtract out stock-based compensation. That is why EBIT is so much decrease.

Checkpoint 3: 2027 EBITDA Margin

Yemi Okupe’s Steerage:

Our expectation is that we are going to obtain adjusted EBITDA margins of no less than low to mid-teens by 2027.

I feel that is cheap and so I forecasted the midpoint of steering with an anticipated EBIT margin of seven%, which is just about in keeping with a mid-teen adjusted EBITDA margin.

Checkpoint 4: 2030 EBITDA Margin

Yemi Okupe’s Steerage:

Our long-term adjusted EBITDA margin targets are 20% to 30%… our expectation is that advertising and marketing as a proportion of income shall be within the mid-30s to low-40s by 2030.

I’ve EBIT in 2030 to be $712 million, which equates to a 15% EBIT margin, which can fall someplace in Yemi’s goal vary for adjusted EBITDA margin.

I feel Hims may have decrease gross margins sooner or later, which might put extra stress on them to chop again on promoting. Proper now, this isn’t essential as a result of there aren’t sufficient reputable opponents to pressure Hims to be extra aggressive on pricing. As that adjustments, I feel Hims may very well be pressured to scale back promoting spend to conjure up a revenue, which in flip, may stifle their future gross sales progress.

So, I did two issues:

I lowered SGA expense to firm steering. I slowed gross sales progress barely extra aggressively, beginning in 2028.

Vertical Line

You will observe a vertical line marking the division between the years after 2027. From 2028 to 2030, I maintained the identical base charge enchancment in SGA. Nevertheless, I then utilized a multiplier of 0.9x to account for a ten% discount in advertising and marketing as a proportion of income. Subsequently, through the interval from 2030 to 2033, I utilized a extra aggressive strategy, utilizing a multiplier of 0.8x to mirror Yemi’s steering that advertising and marketing as a proportion of income will finally fall within the mid 30% vary.

Checkpoint 5: Gross margins

Yemi Okupe’s Steerage:

Over time, we view gross margins going to extra of the mid to high-70s… the trail to type of the mid-70s that we have guided to is certainly going to be in all probability extra of a multiyear journey like that is not going to occur over the course of like a few quarters.

Yemi’s optimism could also be overlooking some potential challenges. Whereas it is tempting to imagine that the corporate’s favorable situations will persist into the longer term as Hims presently outpaces opponents within the telehealth sector by varied key measures, it might be unrealistic to anticipate such excessive margins indefinitely.

An business by which an organization is producing 82% gross margins is prone to appeal to many different suppliers, thus driving down worth. As competitors within the telehealth market intensifies, I anticipate that firms inside this house will start providing related merchandise, with service high quality turning into the first differentiating issue. Nevertheless, enhancing service sometimes entails higher prices in comparison with product differentiation.

Merely warning traders of a decline from 82% to 75% in revenue margins might not suffice. Given the potential for additional erosion, traders may anticipate extra substantial margin decreases. To undertake a extra conservative strategy, I’ve created a glide path right down to 70%, fairly than stopping at 75% as in Yemi’s steering.

Checkpoint 6: 2033 Gross sales

Andrew Dudum’s Steerage:

We predict we’re constructing a $10-20 billion firm.

Whereas Hims’ administration has not set any expectations for gross sales in 2033, CEO Andrew Dudum has explicitly acknowledged he sees Hims as a $20 billion firm.

If Hims generates $6 billion in gross sales in 2033, as in my forecast, it could necessitate a P/S ratio of about 3.3x to be a $20 billion firm. All of those numbers are cheap.

Honest Share Worth

Factoring in administration’s full steering, my very own forecasts, and a few conservatism, Hims’ justifiable share worth is $24.46. This represents potential upside of 62% from at the moment’s present degree of $15.12 per share.

Zooming Out

In any discounted money movement evaluation, the final step includes zooming out to view the large image.

To handle the query of whether or not projecting gross sales to be $6 billion is overly bold or not, I can basically reframe it as, ‘Will Hims change into a 7x bigger firm in 10 years?’

Effectively, to place this in perspective, gross sales must develop at a CAGR of 24% for Hims to be a 7x larger firm in 2033. I feel most would agree that is properly throughout the realm of risk.

So, sure, my DCF is affordable within the massive image.

A Lesson in Zoology with DocShah

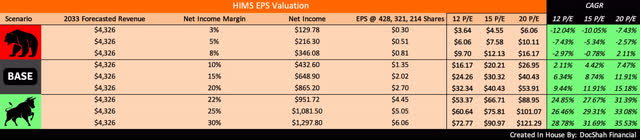

DSF HIMS EPS Desk (DocShah Monetary)

We will additionally worth firms utilizing EPS as an alternative of FCF. Within the above chart, we’ve got a bear case, base case, and bull case. I made a number of assumptions:

Bear Case: Share depend will increase by 2x to 428 million

Base Case: Share depend will increase by 1.5x to 321 million

Bull Case: Share depend stays the identical at 214 million.

The handy factor about the best way I constructed this desk is it permits you, the reader, to rapidly choose all of your assumptions and give you your individual justifiable share worth.

For instance, let’s say you’re impartial on the corporate and consider:

Web revenue margins shall be 15% Shares excellent are 321 million Market assigns a 15 P/E

Then, the inventory can be price $30.32, which represents a CAGR of 8.74% per 12 months from present ranges.

I’d like to know which end result you forecast so let me know within the feedback under. Additionally, please perceive these forecasts are common ranges.

Potential Catalysts

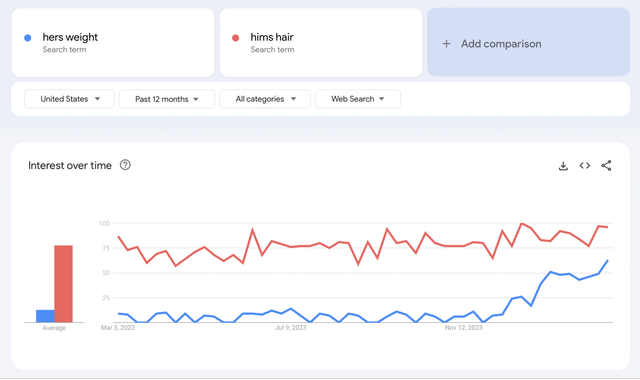

These are under no circumstances sidenotes, however this text is already fairly lengthy. MedMatch, which is Hims’ AI software program that makes use of machine studying and leverages knowledge factors from its sufferers, and the brand new Hers Weight Loss class may each present immense worth to the corporate’s market cap. Nevertheless, as of proper now, I’d say each are presently of their infancy phases, which makes it tough for me to precisely put a price on them. So, within the spirit of prudence, it’s greatest I wait just a little little bit of time to quantify their affect till they endure extra develop. Nevertheless, I needed to no less than acknowledge these catalysts and can start factoring them into forecasts as they each mature. I do assume each MedMatch and Hers are “ready within the wings” and am excited to see them mature.

Hers Weight Google Traits

Google Traits Comparability: Hers Weight vs. Hims Hair (Google)

As a fast illustration of my level that Hers is a sleeping big, have a look above on the Google Traits from the previous 12 months. ‘Hers weight’ may be very rapidly approaching the identical search curiosity as ‘Hims hair,’ one of many firms hottest classes.

Get Off My Garden

I’m going to handle some frequent arguments about Hims folks are likely to yell in fury to see if any maintain validity.

Hims has no moat…

Those that declare Hims has no moat couldn’t be additional mistaken. Initially, the worth proposition supersedes the moat. Buyers who fixate on the latter are “placing the cart earlier than the horse.” It’s akin to complaining about outcomes with out specializing in the method. That is one thing that will get ingrained in you from a younger age while you’re an athlete, which by the best way, I’m an expert baseball participant too.

Second, you may declare any firm doesn’t have a moat of their first few years. What moat did Netflix have when it began?

What made Netflix particular was its worth proposition. Particularly, Netflix’s worth proposition was that it was:

Simpler to make use of Extra handy Earlier to market (maybe extra a aggressive benefit, however why break up hairs) More economical Had higher branding Had customer-friendly insurance policies.

Over time, the corporate expanded upon its worth proposition by including streaming, unique content material, video games, and so forth. It’s precisely this worth growth that’s what traders unknowingly consult with as a moat.

By the best way, if the listing above sounds acquainted, that’s as a result of it ought to. All of these worth propositions may be utilized to Hims.

Particularly, Hims’ worth proposition is that it supplies a 24/7, digital well being and wellness service for nervous/anxious individuals who desperately want these companies, however want to, by nature, keep away from assembly in particular person for stigmatized healthcare considerations. The customized formularies, vertical integration, unbelievable branding, ease of use, comfort, and ease, all present the mandatory basis for an amazing consumer expertise.

Over time, the corporate’s worth proposition will create a recognizable moat. Then, if one other firm needs to compete for market share, it should prime Hims’ worth proposition, not cross its moat.

CAC this, CAC that…

I feel we have to put buyer acquisition price in perspective. Hims is an organization that has:

65% YoY income progress 82% gross margins $221 million in money $0 in debt 14% inside possession Founder led Huge, as in extraordinarily huge, TAM Thousands and thousands of followers throughout socials Retired 237,000 shares for $2 million at $8.42 common worth per share.

But, some traders select to fixate on buyer acquisition price as if it negates all the above. If the corporate’s progress was unfavorable, then I’d say excessive buyer acquisition prices flip from benign to malignant.

I can have a look at any firm on the planet, discover one explicit unfavorable, fixate after which write a PhD dissertation on it. This might be a mistake, as, going again to my earlier level, investing is primarily psychological not logical. There’s a vital change going down in society on how youthful generations want to entry healthcare. A excessive buyer acquisition price in a sea of nice fundamentals will not be going to halt that dynamic from progressing.

Pondering a excessive CAC will blockade this tsunami of a societal shift going down in healthcare is like worrying {that a} pebble will block a river from reaching the ocean.

The very fact is that Millennials and Gen Z have radically completely different psyches that no telehealth firm has recognized and focused the best way Hims has carried out. Additionally, anybody who is aware of promoting will inform you that advertisements change into exponentially costlier the extra focused they’re, so it is sensible that Hims’ extremely focused campaigns are certainly, costly. If this pursuit of the right buyer, costly as it’s, brings in sticky sufferers who pay month after month, then the juice is well worth the squeeze.

90% + of income is recurring income…

Talking of shoppers who pay month after month, Hims doesn’t have me satisfied on their reported recurring income proportion. The one cause I’m just a little suspicious is in the event you have a look at the iOS App retailer (or the web), there are lots of 1 star buyer critiques claiming that the corporate both received’t cancel their subscriptions or that the subscription reveals cancelled, however nonetheless costs them month after month.

Are these gross sales in error labeled as recurring income? If I make and cancel a subscription in January, however then get billed in error one time in my lifecycle in February and/or March, have I became a recurring buyer? I’m unsure.

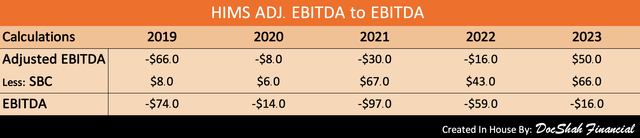

Adjusted EBIDTA… *sigh

HIMS Adj. EBITDA vs. EBITDA (DocShah Monetary )

One of many massive issues with adjusted EBITDA is that it contains stock-based compensation. Due to this fact, the upper SBC is, the upper adjusted EBITDA is, and alas the issue begins to change into apparent: the extra you improve SBC, the extra profitability you painting.

Does this dynamic precisely illustrate a enterprise’ profitability? If we settle for that SBC is an expense to shareholders (which it’s), then how does one logically reconcile growing a value (SBC) will increase your revenue (adjusted EBITDA)?

One can’t as a result of it is unnecessary.

So, we’ve got to take away SBC with a purpose to convert from adjusted EBITDA to EBITDA. So far as the shareholders are involved, it is evident that Hims remains to be producing unfavorable EBITDA, as these earnings are offset by administration’s ever growing compensation.

By the best way, in case you’re questioning, adjusted EBITDA primarily serves as an analysis metric in non-public fairness, fairly than for public shareholders searching for to precisely assess future money flows. Whereas Hims may be extra accustomed to that realm, I consider emphasizing free money movement as an alternative of adjusted EBITDA of their earnings calls can be extra useful.

Dangers

Please perceive there are vital dangers to investing in Hims and Hers Well being. The corporate has nonetheless not confirmed one full 12 months of profitability and there’s no assure it is going to. Buyers have to be ready for the worst-case state of affairs and miscellaneous dangers. I’ll contact on a number of necessary ones under.

Low Barrier to Entry

The telehealth house is a aggressive atmosphere and as such, first to market benefit might not maintain a lot significance. Many traders focus on the specter of Amazon stealing market share away from Hims. Whereas Amazon would definitely be a competitor, the longer Hims continues to ship excellent buyer worth, the extra probably that menace turns into alleviated.

Enjoyable reality – my first ever article for Looking for Alpha was for Dick’s Sporting Items (DKS). It was additionally my largest ever place on the time ($25,000) and I bear in mind my dad pondering I used to be loopy, however I had carried out the analysis and knew the inventory’s intrinsic worth. Again then, the inventory was hammered right down to $23 per share on fears Amazon was going to place them out of enterprise. It was absurd – you had an organization with 70 years of operations, constant EPS progress, founder led (son led at that time), $164 million in money, and no debt – you may see the place the inventory worth is now. Spoiler: it is virtually change into a 10-bagger. The purpose of this anecdote is that Amazon doesn’t crush each enterprise it competes with simply because it is Amazon.

Regulation

Authorities regulation runs rampant within the healthcare business and can probably unfold to the telehealth business, which may considerably disrupt HIMS’ enterprise operations.

Inventory Based mostly Compensation

Extreme stock-based compensation dilutes shareholders from materializing future income after they [the shareholders] have made such vital investments of time and capital.

Fad Picture

The corporate’s vibrant and cheerful branding might not translate properly in sustaining its effectiveness because it expands into completely different markets and demographics. In its current state, some might argue that its branding may very well be perceived as overly informal for severe well being points.

Lawsuit

Hims may get sued sooner or later, maybe for a psychological well being associated misdiagnosis. Relying on the small print of the case, it may very well be expensive for shareholders. Hims distributes so many psychological well being prescriptions, it runs the chance of doubtless prescribing somebody or one thing in error.

10-Okay

For the corporate’s set of dangers, please click on right here.

Takeaway

Hims and Hers Well being is on the forefront of a major societal change going down. Thus far, the corporate has recognized, capitalized, and executed on this pattern and I anticipate that to proceed.

You’ve got heard sufficient in regards to the financials and fundamentals. It is time to actually be an astute investor and give attention to the underlying psychology of the issue Hims is fixing.

Millennials and Gen Z want healthcare, however not if it includes assembly one other human being in particular person. This is not going to change anytime quickly and to this point, Hims solves this dilemma higher than any competitor.

What’s probably the most Millennial/Gen Z approach I can finish this piece?

One thing one thing one thing *insert rocket emoji and shifty eyes emoji right here.

[ad_2]

Source link

(ADBE)")

{kind=link}