[ad_1]

tumsasedgars

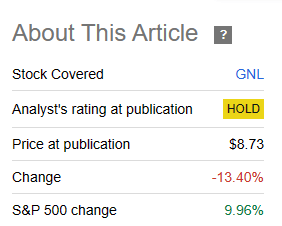

On our final protection of World Internet Lease, Inc. (NYSE:GNL), we spoke in regards to the causes we exited the frequent shares in a well timed style. We additionally lined the popular shares, that are listed under.

World Internet Lease, 7.25% Collection A Cumulative Redeemable Most popular Inventory (NYSE:GNL.PR.A) World Internet Lease 6.875% Collection B Cumulative Redeemable Perp Most popular Inventory (NYSE:GNL.PR.B) World Internet Lease, Inc. 7.50% Collection D Cumulative Crimson Perp Most popular Inventory (NYSE:GNL.PR.D) World Internet Lease, Inc. 7.375% Collection E Cumulative Most popular Inventory (NYSE:GNL.PR.E)

We finally instructed investor keep on with bonds as they have been possible the perfect wager.

That mentioned, when you actually need to take an funding in GNL, the bonds are nonetheless the perfect relative wager. They’re yielding about 8% to maturity proper now on the 2027 notes and we expect GNL ought to make it via that hump (the corporate, not the present dividend) with no points. That’s what we’d deal with.

Supply: 15.66% On Widespread Or 8.50% On Preferreds?

Within the two and half months, the corporate has dropped like a stone and reset the dividend charge and AFFO expectations.

In search of Alpha

We inform you why issues are getting riskier for buyers.

This autumn-2023

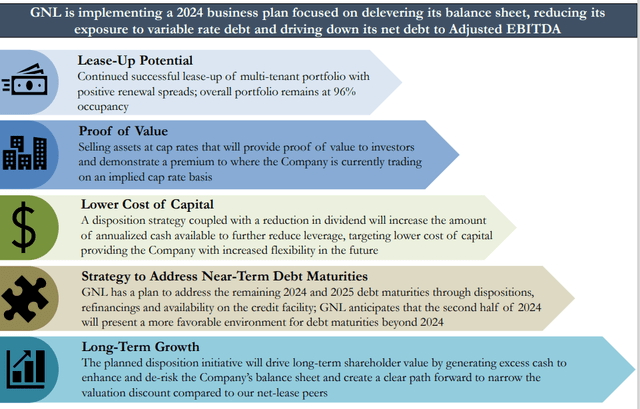

GNL lately accomplished its merger with RTL and the quarter was extremely noisy. That mentioned the corporate reiterated its pre-merger technique.

GNL Presentation

One notable factor right here is that GNL, after years of buying serially with out regret is now trying to dispose belongings. On the entire, we expect these trades over the total cycle can be massively worth harmful. Most of those properties have been acquired throughout ZIRP (zero rate of interest coverage), by both GNL or RTL and promoting now will include far decrease costs. GNL confirmed that the money cap charge on these can be within the 7-8% vary.

So why the change in tune after the last decade lengthy shopping for binge?

You in all probability noticed why whenever you learn the assertion.

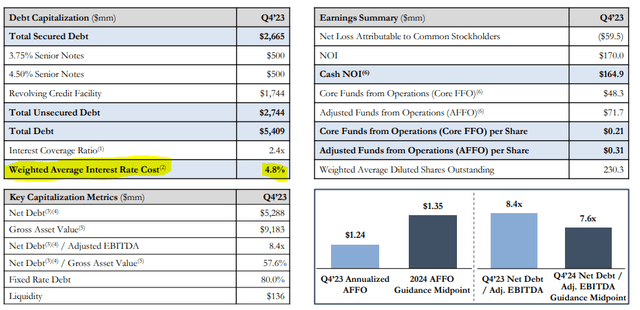

Our internet debt to adjusted EBITDA ratio was 8.4 occasions. We ended the quarter with internet debt of $5.3 billion at a weighted common rate of interest of 4.8% and have liquidity of roughly $135.7 million and $206 million of capability on the credit score facility. The weighted common maturity on the finish of the fourth quarter 2023 was 3.2 years with minimal debt maturity due in 2024. Our debt contains $1 billion in senior notes, $1.7 billion on the multicurrency revolving credit score facility and $2.7 billion of excellent gross mortgage debt. Our debt was 80% mounted charge, which incorporates floating charge in-place rate of interest swaps and our curiosity protection ratio was 2.4 occasions.

Supply: GNL This autumn-2023 Convention Name Transcript

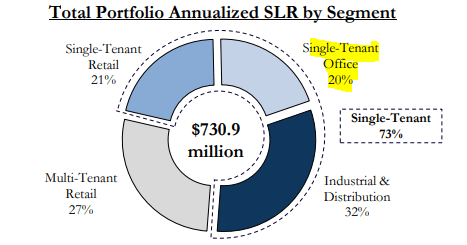

That 3.2 years is the issue and it is going to be a much bigger downside for its belongings within the single tenant workplace class.

GNL Presentation

GNL in fact disagrees that this can be a problem.

One of many metrics that differentiates GNL’s single-tenant workplace portfolio is that it is comprised of 70% mission-critical services, which we outline as headquarters, lab or R&D services and have 68% investment-grade or implied investment-grade tenants, which we consider supplies our portfolio with hire stability and low degree of default threat. Given GNL’s profitable monitor report of lease renewals, the single-tenant workplace phase additionally consists of restricted near-term lease maturities, minimizing the chance of emptiness.

Supply: GNL This autumn-2023 Convention Name Transcript

However when your debt to EBITDA is in that vary, you do not want quite a lot of vacancies to maneuver the stress.

2024 Outlook

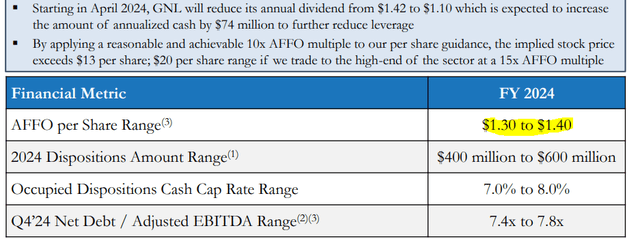

The AFFO is now anticipated to be round $1.35.

GNL Presentation

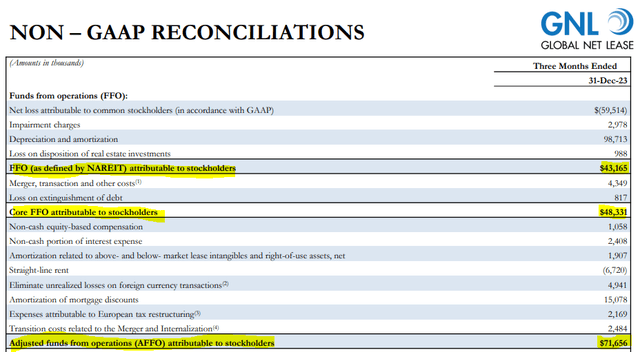

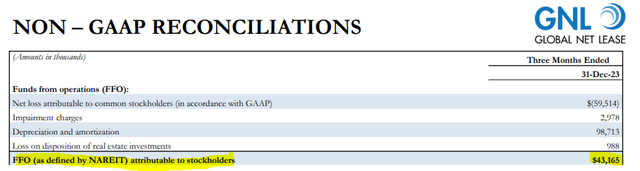

The humorous side right here is that almost all analysts nonetheless present FFO anticipated at round $1.10 per share. This might typically not make sense as analysts won’t ignore administration steerage to such an extent. However the confusion for buyers (not analysts) stems from the truth that GNL is speaking about AFFO whereas analysts are centered on FFO. In most REITs, AFFO tends to be decrease than FFO. Whereas there isn’t a normal definition of AFFO on the US facet (Canadian REITs are extra in step with this), typically AFFO includes lowering the FFO down by upkeep capex and straight line hire. Within the case of GNL, as seen in This autumn-2023, AFFO was considerably greater than FFO.

GNL Presentation

GNL expects an analogous delta for all the yr 2024. We’ll go away it as much as the readers to determine what truly is the actual measure of proprietor’s equal earnings however these “one-time” changes have been a daily characteristic for GNL.

Our Outlook

GNL believes that 15X AFFO is feasible.

As we have taken a conservative method, our technique for deleveraging is designed to be earnings impartial with the expectation that our internet debt to adjusted EBITDA will lower by roughly 1 full flip. By making use of an affordable and achievable 10 occasions AFFO a number of to our per share steerage, the implied inventory worth exceeds $13 per share, $20 per share vary if we commerce to the excessive finish of the sector at a 15 occasions AFFO a number of.

Supply: GNL This autumn-2023 Convention Name Transcript

Realistically, when you may have W. P. Carey Inc. (WPC), Agree Realty Company (ADC) and Realty Earnings (O), buying and selling at a mean of 13X FFO, we’d pay about 7X FFO for GNL after we received the lottery and 5X earlier than. Word that we mentioned FFO and never the fluffed up AFFO quantity. So at $7.50 (contemplating now we have not received the lottery), GNL seems costly. The brand new dividend of $1.10 is near a 100% payout ratio on the now anticipated FFO. This FFO is supposedly bumped up by all the varied synergies anticipated. However the one factor buyers have to deal with right here is that the weighted common rate of interest continues to be from the ZIRP period.

GNL Presentation

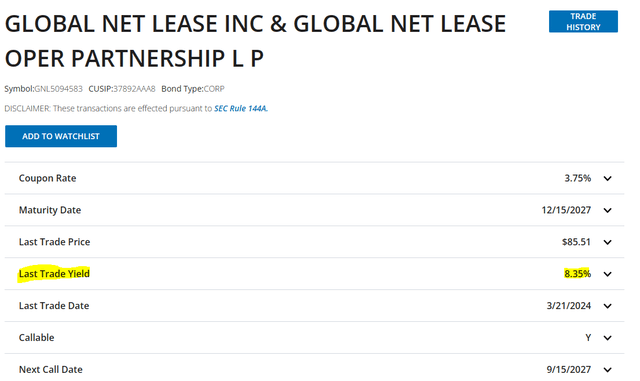

Any affordable repricing of this over the following 3 years can imply quite a lot of points for the corporate. Traders may suppose we’re being overly cautious, however simply take a look at the information. We’ve got had the largest easing of credit score circumstances for the reason that finish of the worldwide monetary disaster. Regardless of that, GNL”s close to time period bonds yield 8.35% to maturity.

FINRA

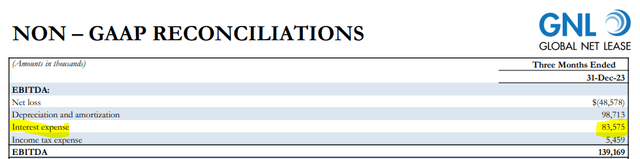

GNL is in fact paying the coupon charge on that however simply think about when you reprice this complete deck to even 7.2% from 4.8%. That could be a 50% improve, however pretty affordable assumption until we return to ZIRP. It isn’t laborious to seek out or to do. There may be the This autumn-2023 curiosity expense.

GNL Presentation

50% of that’s about $42 million. So when you extract $42 million out of current FFO, you will not be left with loads.

GNL Presentation

Verdict

In fact that reset is a very long time away however every little thing now we have seen exhibits that GNL’s base charge of FFO will decline over time. So by the point we get to that 2027 maturity issues might look even worse. GNL must get the leverage down and Fitch’s line within the sand would require quite a lot of FFO lowering asset gross sales.

Components that might, individually or collectively, result in unfavourable score motion/downgrade:

–Lack of fabric enhancements in EBITDA and discount of debt such that Fitch expects the mixed entity’s leverage above 8.0x on a sustained foundation;

–Lack of significant enhancements in governance such that Fitch expects capital entry to stay constrained for the mixed entity on the ‘BB+’ score degree.

Supply: Fitch

In all of this, now we have the popular shares buying and selling truly greater than after we final wrote about this. They presently yield round 8.3% collectively. We consider they signify a really excessive threat relative to that yield. As we had proven lately, you will get 7%-8% yields with nearly zero credit score threat over a 5-7 yr horizon. With GNL, your credit score threat is much greater than even implied by their credit standing in our opinion. So the 8.3% yield is simply too low. If we have been getting 10%-12% that will be a distinct matter. Traders can lose loads in most well-liked shares. These utilizing the one line thesis “Regulated, Ergo Protected” for CorEnergy Infrastructure Belief, Inc. (OTCPK:CORRQ) and its most well-liked shares CorEnergy Infrastructure Belief, Inc. DEP SHS REPSTG (OTCPK:CORLQ), discovered that out with a 96% loss. However right here, we’re downgrading all of the preferreds to a Promote.

Please word that this isn’t monetary recommendation. It could look like it, sound prefer it, however surprisingly, it isn’t. Traders are anticipated to do their very own due diligence and seek the advice of with an expert who is aware of their aims and constraints.

[ad_2]

Source link

")

{kind=link}