Heading into 2024, I argued strongly that the selloff in Tesla, Inc. (NASDAQ:TSLA) shares was set to speed up, as I identified a number of elementary headwinds for the world’s main electrical car (“EV”) firm. Particularly, I identified 4 core arguments: Firstly, on a macro degree I highlighted a normal downturn within the electrical car market, with gross sales numbers in 2023 failing to fulfill excessive progress expectations. Secondly, I voiced concern on elevated competitors from Chinese language EV producers like BYD Firm (OTCPK:BYDDF), that are experiencing rising demand each domestically and internationally. Thirdly, I mentioned the damaging margin impression of Tesla’s up to date pricing technique, in addition to strain from uptrending labor prices within the U.S. Lastly, I pointed to challenges reminiscent of fading investor belief, exacerbated by Elon Musk’s statements on needing new incentives for AI know-how growth and the information of Hertz rebalancing its fleet in direction of inner combustion engine automobiles.

I concluded:

Whereas I anticipate Tesla to report This fall 2023 outcomes broadly according to consensus estimates, referencing $25.75 billion in revenues and 0.75 cents EPS, I see a big draw back threat for commentary on 2024 steerage.

Certainly, Tesla’s This fall outcomes had been reported carefully according to consensus expectations, with $25.2 billion in quarterly gross sales and 71 cents of earnings, whereas the steerage for 2024 crushed bullish hopes. Within the This fall reporting, Tesla administration highlighted that quantity progress in 2024 is predicted to be “notably decrease” in comparison with 2023, seemingly suggesting that supply progress will drop to 10-15% YoY in 2024. Evidently, that is a lot decrease than Elon Musk’s bullish expectations of a long-term 50% supply CAGR set in late 2020. In the meantime, as the amount tailwind is fading, the expansion thesis can also be combating little upside on pricing.

As a consequence, and according to my thesis, Tesla’s selloff in early 2024 did speed up: For the reason that begin of the yr, TSLA shares are down about 33%, in comparison with a bullish 9% acquire for the S&P 500 (SP500).

Searching for Alpha

… As Q1 2024 Deliveries Badly Miss Expectations

As I anticipated, the damaging This fall 2023 momentum has been carried into Q1 2024. On April 2nd Tesla reported manufacturing and deliveries quantity for the Q1 quarter, badly lacking consensus expectations and revealing the primary YoY drop in supply quantity for the reason that early quarters of the Covid pandemic. Throughout the interval from January to finish of March, Tesla delivered solely ~387,000 items, down 9% YoY in comparison with the identical quarter in 2023. In comparison with consensus expectations, Tesla’s supply numbers missed by 40,000-45,000 items, in keeping with knowledge compiled by Refinitiv.

Whereas Tesla argued that decline in quantity was partially as a result of provide chain disruptions (emphasis added) …

Decline in volumes was partially because of the early part of the manufacturing ramp of the up to date Mannequin 3 at our Fremont manufacturing facility and manufacturing facility shutdowns ensuing from transport diversions attributable to the Pink Sea battle and an arson assault at Gigafactory Berlin.

Tesla Q1 deliveries

… I’d level out that the deliveries miss seems extra like a demand-side drawback than a supply-side drawback. Particularly, I spotlight that as a consequence of the manufacturing vs. deliveries mismatch, Tesla has reportedly began to selectively, however aggressively reduce costs (once more).

If the deliveries miss would have certainly been as a result of provide constraint, than costs ought to have enhance, as consumers would attempt to push by way of restricted provide. On value cuts, TechCrunch famous (emphasis mine):

Many long-range and efficiency Mannequin Ys are actually promoting for $5,000 lower than their unique value, whereas rear-wheel drive variations are seeing even greater cuts of greater than $7,000.

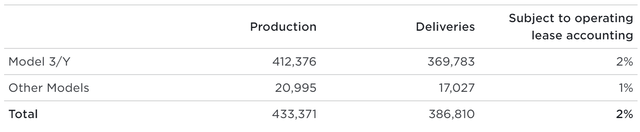

The reductions come as Tesla as soon as once more made much more automobiles than it offered within the final quarter. The corporate constructed 433,371 automobiles within the first quarter however solely shipped 386,810, seemingly including greater than 40,000 EVs to its stock glut. (A few of these automobiles had been seemingly in transit, although Tesla didn’t say what number of.) The corporate has constructed extra vehicles than it shipped in seven of the final eight quarters, Bloomberg Information famous Friday.

In the meantime, additionally Tesla’s vitality technology and storage enterprise seems to be struggling to protect excessive progress charges: In Q1, Tesla deployed 4,053 megawatts, a rise of solely 4% YoY.

Anchored on decrease YoY automotive quantity of (-9%), paired with an estimated YoY discount in ASP of (-5)-(-10)%, I now mannequin that Tesla’s Q1 gross sales numbers will seemingly fall someplace between $22-23 billion. Tesla’s EBIT will rely on how effectively Tesla managed inflationary strain and OPEX self-discipline (R&D spending on full self-driving, or FSD). In any case, pointing to the manufacturing/ deliveries mismatch, Tesla’s Q1 2024 EBIT will extremely seemingly fall in direction of $1 billion, vs. $2.6 billion in Q1 2023.

Wanting Via The Noise

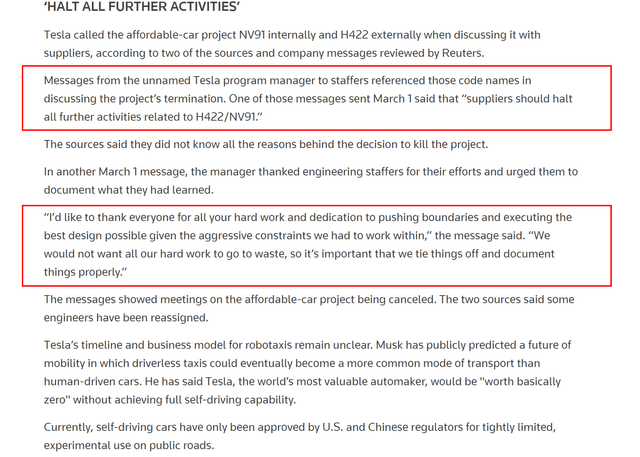

Shortly after the disappointing Q1 2024 deliveries, information broke that Tesla has reportedly reduce its plans to develop/ produce a low-cost automotive. And whereas CEO Elon Musk has been fast to contest the information, I spotlight that the reporting by Reuters has been fairly particular, and thus credible (see under).

Reuters

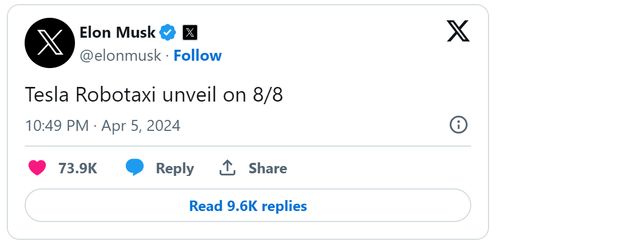

On April fifth, and certain as a counter-balance to the damaging information move referring to the low-cost automotive mannequin, Elon Musk boldly introduced by way of his private X/ Twitter account that Tesla will unveil its Robotaxi product on August eighth. This prompted shares to commerce greater by virtually 4% in aftermarket buying and selling exercise.

X/ Twitter

Nonetheless, buyers ought to take into account that Elon Musk has already teased the potential of Robotaxis inside one yr as early as 2019. As well as, buyers ought to notice that “unveil” occasions don’t point out an imminent industrial launch of a brand new product. Thus, I’m impartial on the implied industrial perspective for Tesla Robotaxis till confirmed in any other case.

Elementary Stress Compounded By Adverse Threat-On Correlation

My overarching, damaging elementary thesis on Tesla as highlighted in my earlier report persists. However on prime of this, right now I now additionally level out an extra, extremely regarding perception on the Tesla thesis. Particularly, I spotlight that for the primary time since COVID, Tesla inventory correlation with risk-on sentiment has turned damaging. To show this, I’ve modelled a correlation evaluation of Tesla shares with the Nasdaq 100-Index (NDX) and Bitcoin (BTC-USD) over the previous 3 years.

To ascertain the relevance of the Nasdaq 100 and Bitcoin as risk-on benchmarks, you will need to notice that the know-how sector (Nasdaq 100) and Crypto are seen as frontiers of innovation. This modern side could be notably interesting throughout “risk-on” durations when buyers are trying to find breakthrough investments that might yield excessive returns. Traditionally, each the Nasdaq 100 and Bitcoin have seen durations of serious, outsized value swings in comparison with the S&P 500, or the Dow Jones Index. For context, the Nasdaq 100 and Bitcoin have a beta vs. the S&P 500 of 1.1-1.3 and 1.3-1.8, respectively.

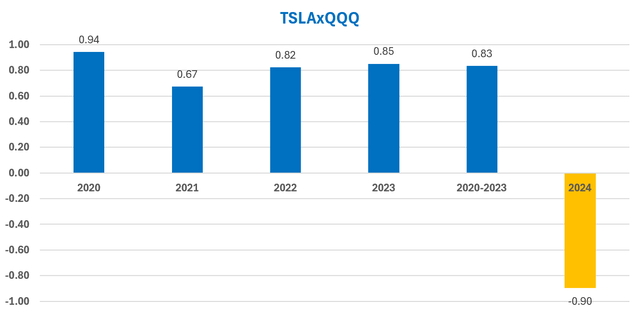

With that body of reference, I’ve mapped the annual correlation of Tesla with each Bitcoin and Nasdaq 100 (QQQ) costs. For context, as a normal rule of thumb:

Very weak correlation: 0.0 to 0.2 Weak correlation: 0.2 to 0.4 Average correlation: 0.4 to 0.6 Sturdy correlation: 0.6 to 0.8 Very sturdy correlation: 0.8 to 1.

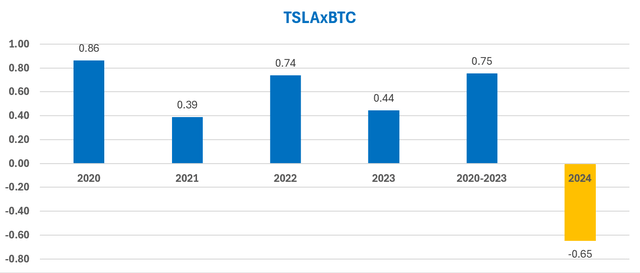

On Bitcoin, I level out that that the TSLA x BTC correlation over the previous 3 years total has been 0.75 (sturdy correlation). Nonetheless, correlation flipped damaging, to -0.65 in 2024 YTD (sturdy damaging correlation).

Yahoo Finance Value Information; Creator’s Evaluation

An excellent stronger correlation sample is clear when mapping TSLA x QQQ: Over the previous 3 years, correlation between the 2 belongings has been 0.83 (very sturdy correlation); however the metric flipped aggressively in 2024 YTD, to -0.9 in 2024 (very sturdy damaging correlation).

Yahoo Finance Value Information; Creator’s Evaluation

The correlation flip for Tesla vs. risk-on belongings is a serious bearish inflection, in my opinion, and the implication on this may hardly be understated. Traders ought to notice that my evaluation implies that Tesla’s inventory is now reacting very otherwise to market sentiment in comparison with the previous, diverging from its earlier alignment with risk-on habits. This might counsel that Tesla has misplaced the good thing about optimistic investor notion, which shielded shares from negativity.

Accordingly, with the sentiment tailwind failing to present assist, Tesla might now be absolutely uncovered to the corporate’s elementary weak point heading into 2024, pointing to arguments highlighted within the intro part of this text. What extra, I see a really seemingly situation the place buyers start (brief)promoting Tesla shares to finance participation in additional dynamic momentum associated to (Gen)AI investments. In truth, that could be a technique that I’ve been pursuing over the previous few weeks.

TSLA Shares May Be Heading As Low As 20x EV/EBIT

With out the optimistic sentiment backdrop that carried Tesla’s sky-high valuation for a number of years, the inventory might be susceptible for a pointy rerating, probably buying and selling right down to the valuation of a typical GARP asset. On that notice, I view a ~$90/ share as cheap, projecting a EV/EBIT of round ~30x. This is able to be a valuation just like the worth a number of seen in Microsoft (MSFT) and Nvidia (NVDA) shares. Nonetheless, assuming the decrease finish the GARP spectrum because the goal, Tesla shares may commerce as little as ~20x EV/EBIT valuation. That is an approximate value a number of seen for Meta Platforms (META), Google (GOOGL), and would counsel a goal value for Tesla as little as ~$60 (my bear case).

Searching for Alpha

Investor Takeaway

Tesla’s selloff is predicted to proceed, as the corporate is dealing with headwinds reminiscent of a downturn within the EV market and elevated competitors from Chinese language producers. On that notice, Tesla’s Q1 2024 efficiency continued the damaging momentum from This fall 2023, with a YoY drop in Q1 supply volumes of 9%, lacking consensus expectations by 40,000-45,000 items. The shortfall in deliveries suggests a good deeper than beforehand anticipated demand-side difficulty, probably bringing Q1 gross sales to $22-23 billion (-3-6% YoY) and EBIT to $1 billion (-60% YoY).

Including to the elemental weak point, I spotlight that for the primary time since COVID, Tesla inventory correlation with risk-on sentiment has turned damaging. The correlation flip is a serious bearish inflection and means that Tesla has lastly misplaced the good thing about optimistic investor notion, which shielded shares from negativity up to now.

With out the optimistic sentiment that carried Tesla’s sky-high valuation for a number of years, the inventory might be susceptible for a pointy rerating, probably buying and selling right down to the valuation of a typical GARP asset. I view a ~$90/ share as cheap, projecting a EV/EBIT of round ~30x. This is able to be a valuation just like the worth a number of seen in Microsoft and Nvidia shares. In step with my correlation evaluation and elementary view on Tesla, I’m downgrading shares to a “Sturdy Promote.”

TERADAT SANTIVIVUT No person can predict if the cycle of acrimonious recriminations between Israel and Iran will cease this week – after the Iranian retaliation for the destroyed...

Richelieu {Hardware} Ltd. (RCH), a number one distributor of specialty {hardware} and complementary merchandise, maintained steady gross sales within the first quarter of 2024, matching the earlier 12...

filo Article Goal Historic outcomes are among the many first issues many traders take into account when analyzing ETFs. Aside from contrarians, traders seek for funds with strong...

By Aatreyee Dasgupta (Reuters) -U.S. Metal shareholders on Friday authorised its proposed $14.9 billion acquisition by Japan's Nippon Metal, as anticipated, taking the merger one step nearer to...

Annually, B-Inventory facilitates the motion of billions of {dollars} value of returned and overstock stock through the world’s largest B2B recommerce market. This implies, in fact, that we...

{kind=link}